Share article on

.svg)

A marketing compliance program is the structured discipline of ensuring that every customer-facing message a regulated business produces — advertisements, websites, emails, social posts, scripts, partner-channel content, finfluencer videos — meets the laws, regulations, and internal policies that govern it before publication, and stays compliant after. In financial services, banking, insurance, and healthcare, it is one of the most consequential operating disciplines a firm runs, and in the past three years it has produced billions of dollars in fines for firms that treated it as an afterthought.

This guide is the definitive 2026 reference: what marketing compliance is, the regulatory frameworks that govern it across industries, what a modern workflow looks like, the violations that draw enforcement, the checklist you can run today, the buyer’s guide for software, the role of AI in 2026, and a comprehensive FAQ.

Marketing compliance is the end-to-end practice of making sure every piece of marketing content a regulated business produces is reviewed, approved, archived, and continuously monitored against the applicable legal and regulatory framework. It is the discipline that sits between the marketing function and the public, and it exists to answer one simple regulator question on demand: show us how you make sure your customers are not misled.

The scope is wider than most teams initially assume. It covers paid advertising, organic social posts, websites and landing pages, blog articles, podcast scripts, video creative, sales-team talking points, customer emails, push notifications, app store screenshots, partner co-marketing assets, and increasingly the content produced by influencers, affiliates, and creators on the firm’s behalf. If a regulated business is the author or sponsor of a communication, that communication is in scope.

These three terms are often used interchangeably and largely overlap, but each has a slightly different emphasis. Marketing compliance is the overall discipline — policies, procedures, controls, archiving, monitoring, governance, and reporting. Marketing review is the pre-publication step within compliance: examining a draft against applicable rules and policies before it goes live. Marketing approval is the act of formally signing off (typically by a registered principal, compliance officer, or designated reviewer) and creating the documented record.

A defensible program produces three deliverables on every covered piece of content: an approve / revise / reject decision, an audit trail showing who reviewed what and when, and an archived copy of the final approved version. For the deeper treatment of how the review step works in practice, see Sedric’s separate pillar on marketing review.

The past three years have produced the most active wave of marketing-related enforcement U.S. and UK regulators have run in recent years. Marketing compliance is no longer a back-office checkbox; it is a board-level risk function with seven- and eight-figure consequences when it fails. A few data points anchor the picture:

The headline fines understate the actual cost of marketing-compliance failure. Industry research consistently finds that the broader impact of a public enforcement action — stock-price reaction, lost revenue, business-disruption costs, regulatory remediation, customer churn, and senior-leadership turnover — typically dwarfs the fine itself. A US$1 million FINRA settlement is rarely a US$1 million event for the business.

The corollary is that the ROI of getting marketing compliance right is asymmetric. Investing in the program is a small fraction of the cost of failing at it, and the firms that have automated the discipline ship campaigns faster than competitors who still review by hand.

Any business whose marketing is governed by sector-specific advertising rules needs a formal marketing compliance program. That is now most of the consumer economy. At minimum, it includes:

If your firm sits in any of these categories, every customer-facing asset belongs in a marketing compliance pipeline — including the long tail of social posts, influencer content, sales-rep LinkedIn updates, partner co-marketing emails, chatbot responses, and app-store screenshots that most programs neglect.

Marketing compliance obligations look different in each sector, but the structural pattern is remarkably consistent across them: a written supervisory procedure, principal pre-approval, content-level testing for fairness and balance, mandated disclosures, recordkeeping, and post-publication monitoring. Below is a working map of the frameworks that drive most U.S. and UK programs today.

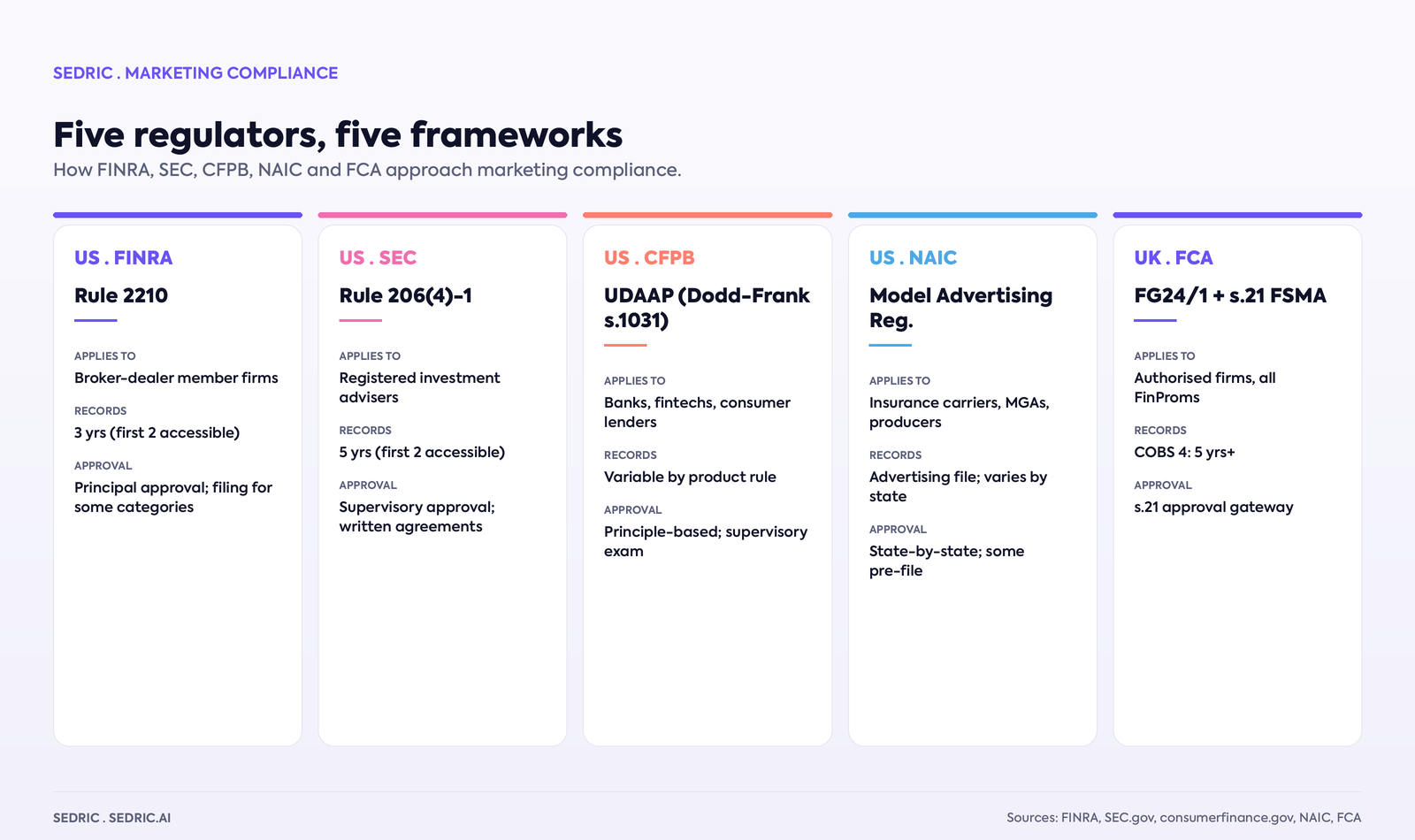

FINRA Rule 2210 is the cornerstone advertising rule for U.S. broker-dealers. It classifies every communication into one of three buckets — retail communications, correspondence, and institutional communications — and applies different supervisory requirements to each. Retail communications generally require principal approval before first use. Certain categories (registered investment companies, options, bond mutual fund volatility ratings) must also be filed with FINRA’s Advertising Regulation Department, often before first use. Rule 2210 sets the substantive bar as well: communications must be fair and balanced, must provide a sound basis for evaluating the facts about any product, and must not omit any material fact whose absence would render the communication misleading. Predictions, exaggerated claims, and selective performance presentations are explicit triggers.

Layered onto Rule 2210 are a series of FINRA Regulatory Notices that extend the same supervisory standard to digital channels: Notice 10-06 (social media), Notice 11-39 (interactive electronic communications), and Notice 17-18 (social-media supervision update, covering third-party content adoption and entanglement plus registered-representative personal social use). For a deeper treatment, see Sedric’s guide on what CMOs need to know about SEC and FINRA ad rules.

The SEC’s amended Marketing Rule consolidated and modernized the old advertising and cash-solicitation rules for registered investment advisers. It introduced a principles-based prohibition on seven categories of false or misleading content; established detailed conditions for testimonials and endorsements; codified rules for the use of third-party ratings; and set strict requirements for performance advertising — particularly hypothetical, predecessor, and gross-versus-net performance presentations. Compensated testimonials and endorsements are now permissible if the adviser provides clear and prominent disclosure of client/non-client status, cash or non-cash compensation, and any material conflicts. The adviser must have a written agreement with the promoter and oversee the promoter’s communications.

SEC Rule 17a-4 requires broker-dealers to preserve all communications received and sent in connection with the firm’s business as such, for at least three years (the first two readily accessible). The 2022 amendments added an audit-trail requirement and clarified that records may be preserved using either WORM-compliant electronic storage or a qualifying audit-trail system. FINRA Rule 4511 incorporates and extends the same requirements. For SEC-registered investment advisers, Rule 204-2 generally requires preservation of marketing materials for at least five years from last use, with the first two readily accessible.

For banks, fintechs, and lenders, the dominant framework is UDAAP — the prohibition on unfair, deceptive, or abusive acts or practices under Dodd-Frank Section 1031 and the FTC Act Section 5. UDAAP is principle-based and intentionally broad, which means a marketing compliance review must look beyond the literal accuracy of a claim and ask whether a reasonable consumer would be likely to be misled, harmed, or steered into an unfavorable outcome. Layered on top are product-specific rules: TILA / Regulation Z for credit advertising (including triggering-term rules), RESPA for mortgage marketing, the SAFE Act for mortgage-loan-originator marketing, and fair-lending considerations under ECOA and the Fair Housing Act. For a deeper treatment, see Sedric’s analysis on how AI can help tame UDAAP risk.

The FTC Endorsement Guides, substantially revised in June 2023, set the cross-industry baseline for any paid endorser relationship: clearly and conspicuously disclose any material connection between the endorser and the firm; ensure endorsements reflect the endorser’s honest opinions; and avoid representations the firm itself could not make. The 2023 revisions tightened the “clear and conspicuous” standard, expanded liability for advertisers and intermediaries, and added explicit language on social-media disclosures, fake reviews, and incentivized testimonials. For any consumer-facing affiliate or influencer program, the Endorsement Guides are the floor — sector-specific rules build on top of them.

Insurance marketing in the U.S. is regulated primarily at the state level, but most states adopt some version of the NAIC’s Advertisements of Life Insurance and Annuities Model Regulation and the parallel Health Insurance model. Both impose substantive content rules: prohibitions on misleading statistics, mandatory disclosure of material limitations, restrictions on the use of terms like “investment” or “deposit,” and required identification of the insurer. Some states require carriers to maintain an advertising file, certify compliance during market-conduct exams, and pre-file certain advertisements.

For prescription drug, medical device, and health-claim advertising, the FDA Office of Prescription Drug Promotion (OPDP) governs the substantive rules: balanced presentation of risks and benefits, accurate indications, fair-balance disclosure, and appropriate audience targeting. Direct-to-consumer drug ads carry particularly strict requirements. Outside FDA-regulated products, the FTC enforces general truth-in-advertising rules with a heavy emphasis on substantiation of health and wellness claims.

In the UK, the FCA’s financial-promotions regime under section 21 of FSMA prohibits a person from communicating an invitation or inducement to engage in investment activity unless approved by an authorized person or exempt. The 2023 amendments tightened the gateway for s.21 approvers and added specific requirements for high-risk investments and crypto-assets. The Consumer Duty (in force since July 2023) requires firms to act to deliver good outcomes for retail customers — including in their communications, which must be timely, clear, and capable of being understood. MiFID II adds further marketing-communication requirements for in-scope investment firms across the EU.

In June 2023, the OCC, FDIC, and Federal Reserve jointly issued the Interagency Guidance on Third-Party Relationships: Risk Management, replacing prior agency-specific guidance and setting unified expectations across the third-party lifecycle. The guidance is risk-based and flexible, but the supervisory expectation is clear: banks own the risk of their partners’ conduct, including their consumer marketing. For BaaS arrangements, the sponsor bank is accountable for fintech partners’ UDAAP exposure, fair-lending posture, and marketing accuracy.

Every regulated marketer must layer in horizontal rules: FTC endorsement guidelines (including disclosure of material connections with influencers); CAN-SPAM and the Telephone Consumer Protection Act for outbound; the EU GDPR and UK GDPR for data-driven targeting; ePrivacy rules for cookies and tracking; ADA and WCAG accessibility considerations for digital content; and the rapidly evolving state privacy law landscape (CCPA/CPRA, plus parallel laws in Virginia, Colorado, Connecticut, Utah, Texas, Tennessee, Iowa, Indiana, Montana, Oregon, Delaware, and others). Platform rules — Google Ads policies, Meta’s special-ad-category requirements for credit and financial services, TikTok’s creator policies — add another constraint set that, while not regulator-issued, can produce business-disrupting account terminations.

A defensible marketing compliance program is not a Slack channel and a goodwill agreement between marketing and compliance. It is a documented workflow with explicit stages, role assignments, decision criteria, and recordkeeping. The shape of that workflow is broadly the same across industries, even when the underlying rules differ.

Every piece of content enters the workflow through a single intake mechanism. At intake, the asset is classified by type (retail communication, correspondence, institutional, advertisement, sales literature, social post, partner content), by product line, by channel, by audience, and by jurisdiction. Classification drives every downstream decision — what rules apply, who must approve, whether it must be filed, and how long it must be retained.

Reviewers run the content against a defined checklist of substantive rules. In broker-dealer practice that means Rule 2210 standards plus product-specific overlays. In banking it means UDAAP analysis, fair-lending review, and TILA triggering-term checks. In insurance it means NAIC content rules plus state-specific disclosures. The output is a redlined draft and a written rationale for any required changes.

Required disclosures are added or verified: risk disclosures, performance footnotes, sponsor identification, “past performance is not indicative of future results,” APR/APY mechanics, lender NMLS identifiers, FDIC-insurance status, regulatory disclaimers. This is the stage at which the most quietly serious issues are caught.

Most regulatory frameworks require approval by a designated, qualified individual: a registered principal in broker-dealer practice, a designated compliance officer in RIA practice, an officer in some state insurance regimes. The approval must be documented, not implied.

Some communications require pre-use or post-use filing with a regulator — FINRA’s Advertising Regulation Department, certain state DOIs, the FCA in some scenarios. The workflow tracks which assets require filing, generates the submission package, and records the regulator’s response.

The approved version is the only version that goes live. The full record — original draft, every revision, every reviewer comment, the approval signature, and the final published asset — is captured in a tamper-evident archive that satisfies the firm’s recordkeeping rule.

Modern enforcement increasingly focuses on what happens after publication — what partners actually said, how landing pages drifted from the approved version, what edits creators made on platforms the firm doesn’t fully control. Post-publication monitoring closes the loop with periodic sampling and, ideally, continuous content surveillance across owned and third-party channels.

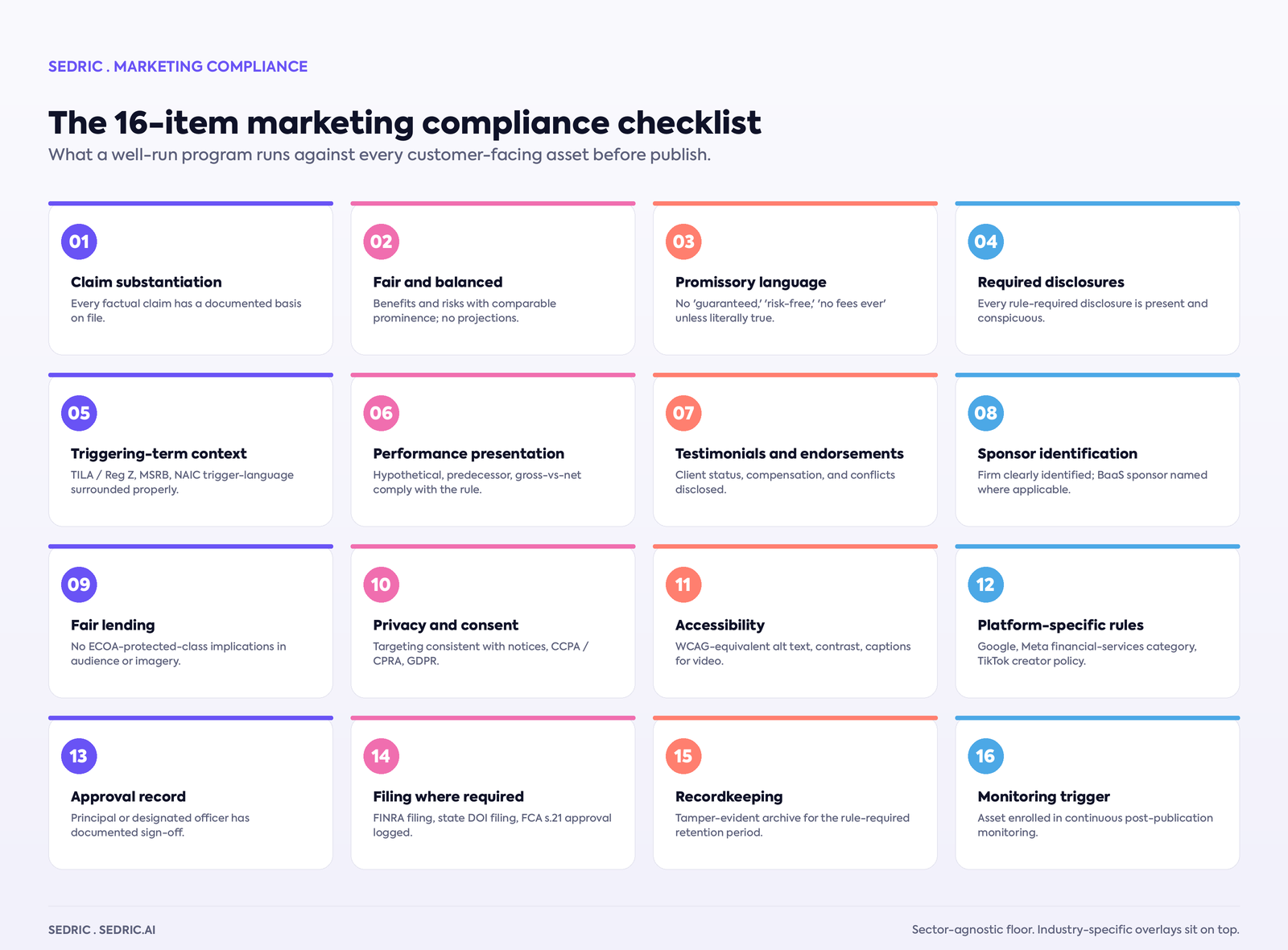

The following checklist is what a well-run program runs against every customer-facing asset before it goes live. It is sector-agnostic; specific industries will layer additional items on top. Use this as the floor.

The same patterns recur across nearly every marketing-compliance enforcement action. Knowing them is half of avoiding them.

Most regulated firms still review marketing content largely by hand: an analyst reads the draft, applies the lexicon and policy in their head, redlines what they catch, and sends it back. That model worked when marketing volume was a few dozen pieces per quarter. It does not scale to a world where a single firm produces thousands of social posts, hundreds of paid ads, dozens of landing-page variants, and a long tail of influencer content every month.

Manual review captures nuance and picks up context human readers spot but rule engines miss. Its limits are obvious: throughput, inconsistency between reviewers, fatigue effects, and the inability to maintain post-publication monitoring at scale. A typical manual queue produces a 3-day-to-3-week turnaround on retail communications, which is the bottleneck most marketing teams describe in customer interviews.

Modern automated marketing compliance applies a structured policy library to every piece of content the moment it arrives, scoring against required disclosures, prohibited claims, promissory framing, and inferential conduct concerns. It runs continuously and consistently, captures the audit record as a byproduct of the workflow, and extends to post-publication monitoring across channels human teams cannot realistically sample.

The mature programs run both. Automation does the first-pass review on 100% of content, surfaces the issues, and triages by risk. Human reviewers focus on the exceptions, ambiguous calls, and highest-risk assets. The cost structure flips: instead of paying for analyst hours roughly proportional to volume, the firm pays a fixed software cost plus a smaller analyst team focused on the genuinely hard reviews. Throughput improves by 5-10x and audit-readiness improves with it.

Marketing compliance has historically been a regular-expression and checklist discipline. A reviewer wrote a lexicon, the system flagged messages matching the lexicon, and a human triaged the flags. That model is being replaced by large language model-based review that reads content the way a senior compliance analyst would, understanding context, inferential meaning, and the substantive intent of the regulator’s rule rather than just the literal phrasing.

AI is reshaping the discipline in four concrete ways:

The risk is real: an AI system trained or deployed carelessly can introduce new UDAAP, fair-lending, or accessibility issues of its own, and regulators have made clear they expect firms to govern AI tooling with the same rigor they apply to any other compliance control. The bar is human-in-the-loop oversight, model documentation, bias monitoring, explainability of every flag, and continuous validation.

If you are evaluating marketing compliance software, the differences between platforms can be hard to surface from a website. The criteria below separate the platforms genuinely built for regulated marketing from the ones that retrofit a generic review workflow.

1. Regulator-tuned policy library out of the box. Does the platform ship with a working policy library for the frameworks your firm is subject to — FINRA Rule 2210, the SEC Marketing Rule, CFPB UDAAP standards, NAIC model regs, FCA financial promotions — or does it expect you to build the rule set yourself?

2. Substantive review, not just workflow. Many “marketing compliance” tools are actually marketing project management with an approval step. The platforms worth buying produce a substantive first-pass review — identifying missing disclosures, promissory language, off-policy claims — before the human even opens the asset.

3. Post-publication monitoring. Pre-publication review without post-publication monitoring leaves the biggest enforcement risk uncovered. The M1, Public.com, Moomoo, and TradeZero finfluencer settlements all traced back to the gap between approved and published.

4. Partner and channel coverage. Does the platform handle the full surface area — first-party marketing, partner co-marketing, affiliate content, influencer posts, sales-rep social, customer-service chatbot output?

5. Audit-ready recordkeeping by default. Every review, every decision, every disclosure check should be captured automatically as a byproduct of the workflow.

6. Explainability of every flag. When the platform flags content, it should produce a rationale tied back to the specific rule and the specific text that triggered the concern.

7. Integration with your marketing stack. Marketers create in Canva, Figma, HubSpot, Google Docs, Adobe, video editors. The platform should meet them where they work.

8. Speed. The compliance-velocity benchmark in 2026 is clearance in minutes for low-risk assets and hours for high-risk ones, with human reviewers focused on exceptions.

9. Multi-jurisdiction and multi-language. If your firm operates across the U.S., UK, EU, or globally, the platform must apply the correct framework per jurisdiction and handle multi-language content.

10. Reference customers in your category. Ask for reference customers in your specific regulatory profile.

For a focused comparison of the leading platforms, see Sedric’s analysis of the top marketing compliance software providers.

The framework outlined above applies across industries, but each vertical has nuances that shape what a compliant program actually looks like.

For banks, UDAAP is the dominant framework; TILA / Regulation Z, RESPA, the SAFE Act, ECOA, and Fair Housing Act overlay product-specific requirements. For sponsor banks in BaaS arrangements, the June 2023 Interagency Guidance on Third-Party Risk Management puts the supervisory obligation squarely on the bank. Sedric’s compliance platform for banks and issuers is built for exactly this profile.

Fintechs inherit the same federal banking framework through their sponsor relationships, plus state UDAP statutes, platform rules (Meta and Google special-ad-category requirements), and the additional scrutiny that comes with high-velocity acquisition marketing. The defining tension is speed: launching campaigns in days, not weeks. See Sedric’s compliance platform for fintechs and neobanks.

The SEC Marketing Rule is the controlling framework: seven categories of prohibited content, strict conditions on testimonials and endorsements, codified third-party rating rules, and detailed performance-presentation requirements. Sedric’s compliance platform for trading and securities firms covers this surface.

Insurance marketing operates on a 50-state matrix layered over the NAIC Advertisements of Life Insurance and Annuities Model Regulation and parallel Health Insurance model. Producer-distributed advertising requires the same supervisory regime that the carrier maintains for its own marketing.

Crypto marketing sits in the most rapidly-evolving regulatory environment in 2026: SEC and CFTC enforcement on promoter relationships, MiCA in the EU, the FCA’s tightened financial-promotions regime in the UK, and state-level money-transmitter rules. See Sedric’s compliance platform for crypto platforms and exchanges.

FDA Office of Prescription Drug Promotion (OPDP) rules govern prescription drug, medical device, and health-claim advertising. Direct-to-consumer drug ads have particularly strict fair-balance and risk-disclosure requirements. HIPAA marketing restrictions apply to communications involving protected health information.

If you are starting a marketing compliance program from scratch or maturing one that has grown organically, the program-level decisions matter more than the workflow itself.

Centralized intake, decentralized creation. Marketers can create across dozens of tools, but every asset enters one intake queue with consistent metadata.

Tiered review by risk. A whitepaper aimed at institutional investors and a TikTok ad aimed at retail beginners need different review depth.

Codified policy library. The rules that govern your industry should live as a structured artifact — a watchlist of risky terms, required disclosures keyed to product and jurisdiction, prohibited claim categories — not as a Word document in a shared drive.

Real-time, not retrospective, surveillance. Quarterly sampling catches problems months after they happened. Continuous monitoring across approved channels, partner channels, and third-party creators catches them in days or hours.

Defensible documentation by default. If recordkeeping is something an analyst has to remember to do at the end of a project, it will fail.

Metrics the regulator will ask for. Average review turnaround time, rework rate, percentage of campaigns shipped on time, percentage of channels under continuous monitoring, time-to-archive, audit-readiness score.

Sedric is an AI compliance platform purpose-built for regulated marketing. Its marketing compliance product sits across the workflow described above — pre-publication review, principal approval, recordkeeping, and post-publication monitoring — and applies a regulator-tuned policy engine to every asset. The platform encodes FINRA Rule 2210, the SEC Marketing Rule, CFPB UDAAP standards, NAIC content rules, FCA financial promotions, MiFID II, and the firm’s own internal policies as a structured rule library, runs every asset against that library, and produces an explainable, auditable decision with a complete record of the inputs.

In practice that means marketing teams get content cleared in minutes rather than days, compliance teams shift from manual reading to managing exceptions, and the firm walks into any regulator exam with a complete, queryable archive of what was reviewed, who approved it, and what was published. Sedric’s broader platform extends the same approach to communications and partner-channel content. For a closer look at the underlying engine, see the AI Reviewer. Book a 30-minute demo and we’ll review your own assets, map findings to your specific policies, and show you what a 5-minute clearance pipeline looks like end-to-end.

Marketing compliance is the structured discipline of ensuring that every customer-facing message a regulated business produces meets applicable laws, regulations, and internal policies before publication, and stays compliant after. In financial services, banking, insurance, and healthcare, it is governed by sector-specific frameworks including FINRA Rule 2210, the SEC Marketing Rule, CFPB UDAAP, NAIC model regulations, FDA OPDP rules, and FCA financial promotions.

Marketing compliance is the overall discipline — policies, controls, archiving, monitoring, and reporting. Marketing review is the pre-publication step within that discipline: examining a draft against applicable rules and policies before it goes live. Marketing approval is the formal sign-off step within marketing review.

Responsibility is shared. The Chief Compliance Officer or designated principal owns the program. Marketing creates the content. Compliance reviews and approves. Legal weighs in on contractual or claims-substantiation questions. The principal’s sign-off is the act that satisfies the rule in most broker-dealer and adviser contexts.

In manual programs, anywhere from two days to three weeks depending on asset complexity, jurisdiction, and team workload. AI-assisted programs routinely cut that to minutes for low-risk assets and hours for high-risk ones, with human reviewers focused on exceptions.

At minimum: the original asset, every revision, every reviewer comment, the approval signature, the final published version, and the dates and identities associated with each. Retention periods vary — three years from last use under SEA Rule 17a-4 and FINRA Rule 2210 for broker-dealers, five years for SEC-registered advisers under Rule 204-2, five to seven years for MiFID II, and longer in some state insurance regimes.

Yes. FINRA Regulatory Notices 10-06, 11-39, and 17-18, the SEC Marketing Rule, and the FTC Endorsement Guides all extend to social posts, influencer content, and content posted by employees on the firm’s behalf. Recent FINRA enforcement (M1 Finance $850K, Public.com $350K, Moomoo $125K, TradeZero $250K) makes clear that firms are responsible for what their paid creators say.

No, and regulators are clear on this point. AI can dramatically accelerate review and apply policy more consistently than humans, but human-in-the-loop oversight, principal approval where required, model governance, and explainability are non-negotiable. AI is the analyst; the principal is still the principal.

The SEC Marketing Rule (Advisers Act Rule 206(4)-1) is the modernized advertising rule for SEC-registered investment advisers, fully effective in November 2022. It consolidated the old advertising and cash-solicitation rules, prohibits seven categories of false or misleading content, establishes conditions for testimonials and endorsements, codifies third-party rating rules, and sets strict performance-advertising requirements.

FINRA Rule 2210 is the cornerstone advertising rule for U.S. broker-dealers. It classifies every communication into retail, correspondence, or institutional, applies different supervisory requirements to each, requires principal approval for most retail communications before first use, and sets the substantive fair-and-balanced standard for all communications.

UDAAP stands for Unfair, Deceptive, or Abusive Acts or Practices, prohibited by Dodd-Frank Section 1031 and the FTC Act Section 5. For banks, fintechs, and lenders, UDAAP is the dominant marketing-compliance framework. It is principle-based and intentionally broad, which means a marketing compliance review must look beyond the literal accuracy of a claim and ask whether a reasonable consumer would be likely to be misled.

In the UK, section 21 of the Financial Services and Markets Act prohibits a person from communicating an invitation or inducement to engage in investment activity unless approved by an authorized person or exempt. The 2023 amendments tightened the gateway for s.21 approvers and added specific requirements for high-risk investments and crypto-assets. The Consumer Duty (effective July 2023) overlays good-outcomes requirements on retail-customer communications.

Marketing compliance software pricing varies materially based on volume, modules, and the firm’s regulatory profile. Enterprise platforms typically range from low five-figure annual licenses for smaller firms to high six-figure or seven-figure programs for large broker-dealers and BaaS sponsor banks. The right comparison is not software cost vs. zero; it is software cost vs. the fully-loaded cost of the analyst hours, rework cycles, and enforcement exposure the platform replaces.

Marketing compliance focuses on pre-publication content the firm produces or sponsors — ads, websites, emails, social posts, partner content. Communications compliance focuses on the ongoing capture, retention, and supervision of every business communication a covered person sends — including the long tail of one-to-one messages over email, chat, and voice. The two disciplines overlap but each has its own regulatory framework.

Run a self-exam against the same questions a regulator will ask: produce the written supervisory procedures, the policy library, the approval records for a sample of assets, the post-publication monitoring evidence, and the metrics summary. The gap between what a firm can produce on a Tuesday morning and what the regulator expects to see is the gap to close before the exam letter arrives, not after.

Marketing compliance is the firm’s answer to a single regulator question: show us how you make sure your customers are not misled. The firms that answer that question well in 2026 have a documented workflow, a codified policy library, continuous post-publication monitoring, defensible recordkeeping by default, and the technology to apply that machinery at the speed of modern marketing. The firms that answer it badly are the ones that pay seven figures to find out their process did not scale. Sedric was built for the first kind of firm.

Convert your static procedures into active AI controllers that protect your brand 24/7.

.svg)

Scale marketing compliance without slowing down.