Share article on

.svg)

TL;DR — Form CRS (Form ADV Part 3 for advisers; equivalent for broker-dealers) is the standardised, plain-English relationship summary every SEC-registered RIA and FINRA-registered broker-dealer must deliver to retail investors. The compliance date was 30 June 2020. Since then, the SEC has run multiple targeted enforcement sweeps focused on three failure patterns: late or missed initial delivery, missing or inaccessible website posting, and content non-conformance to the prescribed format. This guide covers the form's content requirements, the delivery and retention obligations under Rule 204-5 (advisers) and Rule 17a-14 (broker-dealers), the conversation-starter requirements that examiners check for, the public enforcement record, and the operational programme that produces audit-ready evidence on demand.

Form CRS — short for Client (or Customer) Relationship Summary — is a standardised, plain-English relationship summary that SEC-registered investment advisers and FINRA-registered broker-dealers must deliver to retail investors. The form is structured to help retail investors compare advisers, broker-dealers, and dual-registrants on the most consequential dimensions: the services offered, the fees and costs, the standard of conduct, the conflicts of interest, and any disciplinary history.

The form is two pages for firms that operate in a single capacity (adviser-only or broker-dealer only). For dual-registrants — firms registered as both advisers and broker-dealers — the form is four pages and covers both capacities, side by side.

Who must file:

The obligation runs only with retail investors. "Retail investor" is defined as a natural person, or the legal representative of a natural person, who seeks to receive or receives services primarily for personal, family, or household purposes. The form is not required for institutional investors, qualified purchasers in private fund contexts, or other non-retail audiences. Many firms deliver Form CRS to anyone they engage with as a matter of policy because the cost of misclassification is asymmetric.

Form CRS was adopted on 5 June 2019 as part of the Regulation Best Interest rulemaking — the package that also produced Reg BI itself (the new standard of conduct for broker-dealer recommendations to retail customers), the Commission's interpretive release on the investment adviser standard of conduct, and Form CRS as the disclosure layer that bridges the two regimes.

The compliance date was 30 June 2020. From that date, every retail-facing adviser and broker-dealer was expected to be filing Form CRS, delivering it to retail investors, posting it on its website, and maintaining records of delivery.

The form is the SEC's answer to a long-standing problem: retail investors did not understand the difference between an adviser, a broker-dealer, and a dual-registrant, did not understand which standard of conduct applied to which interaction, and did not have a single document to compare firms against. Form CRS is intentionally short, intentionally formatted, and intentionally identical in structure across firms — so retail investors can compare two firms' summaries page-for-page.

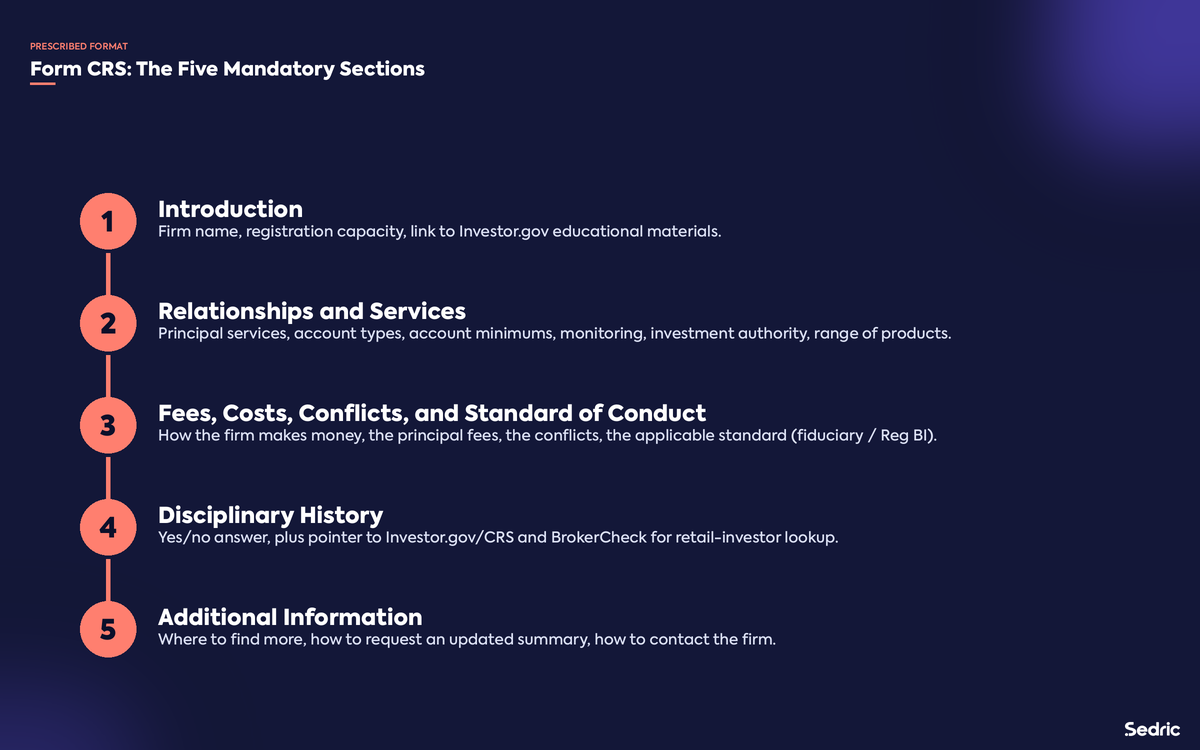

Form CRS uses a prescribed format. The order of sections, the headings, the formatting cues, and the placement of conversation starters are all mandated. Firms have limited flexibility on substance within each section but no flexibility on structure.

Identifies the firm by name, states its registration status (investment adviser, broker-dealer, or both), and tells the retail investor where to find free and simple educational materials about investment advisers, broker-dealers, and investing. The Commission-specified URL is referenced here.

What investment services and advice the firm provides to retail investors. The section must address: the firm's principal services, account types offered, account minimums (if any), monitoring obligations (and any limits on monitoring), investment authority (discretionary, non-discretionary), the range of investments offered, and any material limitations on the services (e.g. proprietary product limitations).

The largest section, covering: how the firm makes money, the principal fees the retail investor will pay, the fees that may apply to specific accounts or transactions, and a plain-English summary of how the fees affect the investor's money over time. Conflicts of interest specific to the firm's compensation model (proprietary product preferences, payment for order flow, revenue-sharing arrangements, third-party compensation) must be disclosed. The standard of conduct that applies — the fiduciary duty under the Advisers Act for advisers, Reg BI for broker-dealers — must be stated plainly.

A yes-or-no answer to whether the firm or its financial professionals have legal or disciplinary history, plus the location of free public-search resources (Investor.gov/CRS and BrokerCheck) where retail investors can research that history themselves. Firms with disciplinary history cannot omit or minimise it; the SEC has been explicit that a "yes" answer with no detail is the required format and that the public search resources do the rest.

Where to find additional information about the firm's services, how to request an updated relationship summary, and how to contact the firm.

The form has prescribed character or word limits within each section to keep the document genuinely two-page (or four-page for dual-registrants). Firms that exceed the limits have to cut content; firms that fall well under do not, but the discipline of the format is the point.

One of Form CRS's distinguishing features is that it must include specific "conversation starters" — questions the form invites the retail investor to ask the firm's financial professional. These are not optional and the wording is prescribed.

The required conversation starters cover at minimum:

Examiners check for the conversation starters in their prescribed locations on the form. Firms that omit one, paraphrase one, or relocate one have produced a non-conforming Form CRS, regardless of whether the substance elsewhere is accurate.

The delivery obligation is the most operationally demanding part of Form CRS compliance, and historically the most-cited in enforcement.

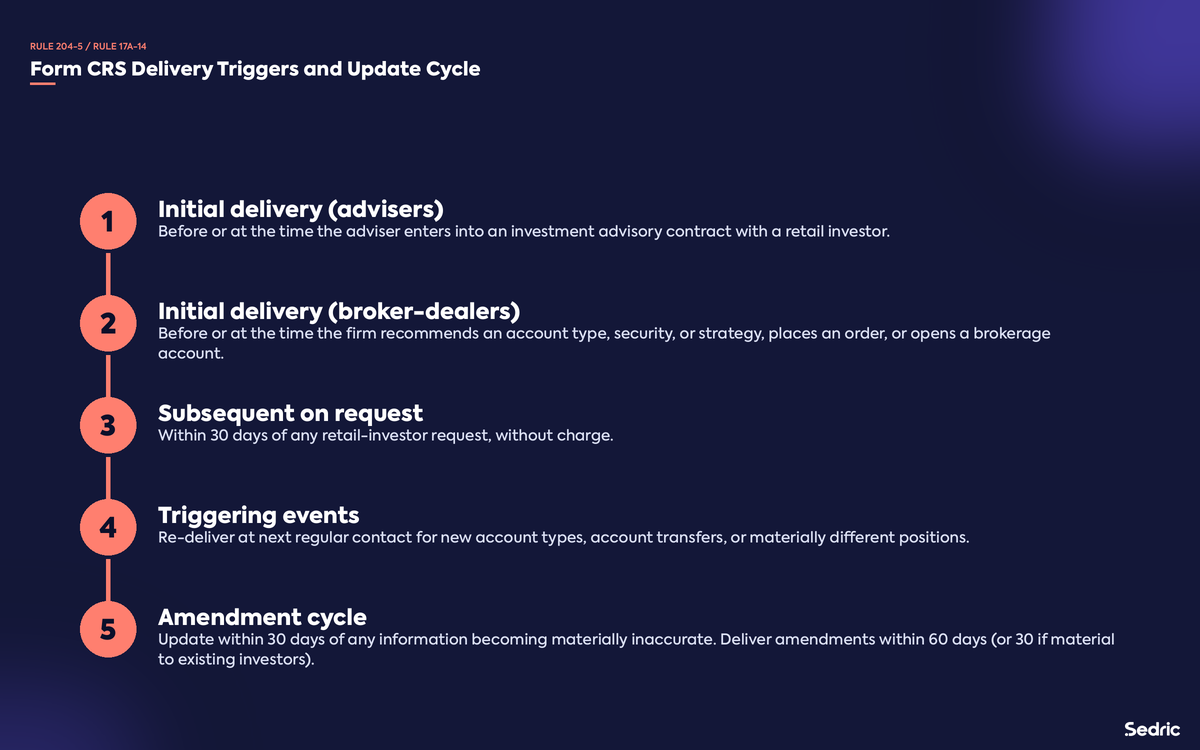

Advisers must deliver Form CRS to a retail investor before or at the time the firm enters into an investment advisory contract with the investor (Rule 204-5(b)(1)). Broker-dealers must deliver it before or at the time the firm: recommends an account type, security, or investment strategy to a retail investor; places an order for a retail investor; or opens a brokerage account for a retail investor (Rule 17a-14).

Dual-registrants must deliver the combined form at the earlier of either trigger.

Delivery may be in paper or electronic format. Electronic delivery is subject to the same consent and access conditions that apply to other regulatory disclosures (the 1996 and 2000 SEC interpretive releases on electronic delivery, and the more recent guidance on default electronic delivery). Firms cannot assume electronic delivery is acceptable in all cases; affirmative consent or appropriate notice procedures must be in place.

If a retail investor requests Form CRS at any later point, the firm must deliver it within 30 days of the request, without charge.

When the firm amends Form CRS in a way that creates a new version, the firm must deliver the updated version to retail investors within 60 days of the amendment, or within 30 days if the change is to information that is material to an existing retail investor.

Form CRS must also be re-delivered to retail investors at the next regular contact when one of certain triggering events occurs — for example, when a new brokerage or advisory account is opened that differs from the investor's existing accounts, when a recommendation involves moving assets to a different type of account, or when a transaction places retail investors in a materially different position with the firm.

If a retail investor has both an advisory and a brokerage relationship with the same dual-registrant, a single combined Form CRS satisfies the delivery obligation for both relationships.

Every firm that must file Form CRS must also post the current version on its public website in a way that is "prominent." The Commission has not prescribed a specific URL pattern, but the SEC has been clear that the form must be discoverable from the firm's main website navigation and accessible without requiring registration or login.

In practice, the most defensible pattern is a top-level navigation link labelled clearly (e.g. "Relationship Summary," "Form CRS," or both) leading to a page that contains either the form itself or a PDF link with the form. Burying the form in a footer-of-the-footer or behind a hover state has been cited as a deficiency.

The website version must match the version filed with the SEC. When the filed version updates, the website version must update within the same delivery window applicable to that amendment.

Form CRS recordkeeping sits under Rule 204-2(a)(14) for advisers and Rule 17a-3(a)(35) and 17a-4(b)(4)(vi) for broker-dealers.

Required records include:

The retention period is five years for advisers (with the first two years in an easily accessible place) and three years for broker-dealers under the standard 17a-4 schedule.

The delivery log is the record examiners typically request first. A firm that cannot produce, on demand, a date-stamped record of when Form CRS was delivered to each retail investor has a Form CRS deficiency regardless of whether the form's content is correct.

Form CRS must be updated within 30 days of any information in the form becoming materially inaccurate. The amended form is filed through IARD (advisers) or CRD (broker-dealers), posted to the website, and delivered to existing retail investors on the schedule described above.

Material inaccuracy is a fact-specific assessment. Common triggers include: a change in the firm's service offerings, a material change in fees, a change in the standard of conduct that applies (e.g. as a result of registration changes), a new disciplinary event involving the firm or a covered financial professional, and a change in the firm's name or contact information.

A firm that operates a continuous compliance calendar tied to Form CRS triggers tends to catch material inaccuracies sooner than one that relies on annual review. Annual review is generally insufficient because Form CRS is a "current state" document and material changes during the year must be reflected within the 30-day window, not at the next anniversary.

Form CRS enforcement has run in identifiable waves. The pattern across them is consistent: examiners are catching delivery failures, posting failures, and content non-conformance, not material misstatements about substance.

The SEC announced settled charges against 27 firms — 21 investment advisers and 6 broker-dealers — for failures to timely file and deliver Form CRS, post the form on their websites, or otherwise comply with the rule's basic delivery and posting requirements. Penalties ranged from low five-figure amounts to over US$100,000 per firm, with total collected penalties in the seven-figure range.

Subsequent settled actions through 2022 and 2023 continued the pattern, with additional firms cited for missed delivery, missed posting, and instances where the form filed with the SEC differed from the version posted on the firm's website. The Division of Examinations has used Form CRS as a routine examination element in adviser and broker-dealer exams.

The Division of Examinations has published Risk Alerts and FAQs throughout the rule's life calling out persistent failures: forms that did not include the required conversation starters in the prescribed locations; firms that posted the form on their website but in a way that examiners found insufficiently prominent; delivery logs that did not specify whether delivery occurred before or at the time of the triggering event; and disciplinary-history sections that minimised or obscured disclosable events.

Form CRS enforcement is rarely about whether the substance is true. It is about whether the form was filed and updated on time, delivered to retail investors on time, posted prominently on the firm's website, and matches the filed version. A firm with a strong operational programme on those four surfaces is largely surviving Form CRS exam questions; a firm without is not.

A defensible Form CRS programme rests on five operational pillars.

The firm should maintain Form CRS in a single source-of-truth system, with version control, change history, and an audit trail of who approved each change and when. The SEC-filed version, the website version, and the delivered version must always be the same version.

Initial delivery should be automatic at the triggering event — account opening, advisory contract execution, recommendation to a retail investor, or whichever applies. The workflow must capture the date and method of delivery and store it as a delivery record. Manual delivery processes invite gaps; automated workflows produce the audit trail examiners ask for.

The website-posted version must update within the delivery window when the form is amended. The most defensible architecture is a single CMS link that resolves to the current PDF, with the PDF object itself versioned and timestamped. Multiple copies of the form scattered across pages create the risk of divergence.

The firm must be able to produce, on demand, the date Form CRS was delivered to each retail investor, the version delivered, and the method of delivery. The amendment tracker must show every amendment, the date it was filed, the date it was posted, and the delivery to existing retail investors that followed.

Records under Rule 204-2(a)(14) (advisers) and Rule 17a-4 (broker-dealers) must be retained for the applicable period (five or three years, respectively) with adviser records in easily accessible form for the first two years. The retention layer should be tested with a mock production request annually.

The first two pillars are where the operational workload sits. The third pillar is where most firms have the largest gap. The fourth and fifth pillars are where the audit trail lives.

Sedric integrates Form CRS into the firm's broader compliance programme. The platform sits across marketing review, communications surveillance, and the supervisory documentation that produces examiner-ready evidence. Form CRS sits inside that programme:

Versioned Form CRS as a source of truth. The current Form CRS, every prior version, the change history, and the approver of record are stored in a single source-of-truth system the firm and the examiner can both audit.

Delivery-trigger integration. When the firm's account-opening, advisory-contract, or recommendation workflows fire, Sedric flags the Form CRS delivery requirement and captures the delivery record — date, method, version delivered, recipient.

Website-posting synchronisation. The Form CRS asset library is integrated with the firm's CMS so the website-posted version stays in sync with the filed version. Divergence is flagged before it can persist for more than a delivery cycle.

Amendment cadence tracking. When marketing-activity or service-offering changes are captured elsewhere in the platform (the Marketing Rule policy library, the supervisory program), Sedric flags downstream Form CRS implications: an updated fee structure triggers a Form CRS amendment review; a new account type triggers a Section 2 amendment; a disciplinary event triggers a Section 4 update.

Audit-ready delivery log. The delivery log is exportable in the form examiners actually request: retail investor identifier, date, method, version. The 5-year retention (advisers) and 3-year retention (broker-dealers) are managed natively.

For dual-registrants, the combined Form CRS workflow is supported alongside the standalone adviser and broker-dealer flows. For firms that have both retail and institutional client bases, the retail-investor classification is captured in the workflow so the delivery obligation runs correctly without manual gatekeeping.

Form CRS applies to SEC-registered advisers with retail-investor relationships. A pure private fund adviser with no natural-person investors outside qualified purchaser arrangements typically has no Form CRS obligation. The fact-pattern matters: an adviser that takes any natural-person retail investors as separately managed account clients does have the obligation.

The federal Form CRS obligation applies to SEC-registered advisers. State-registered advisers are subject to their state regulator's framework. Some states have adopted Form CRS equivalents; most have not. Firms moving between state and SEC registration should plan the Form CRS implementation for the transition date.

The form may be delivered separately or with other onboarding documents, subject to the prominence requirement: the form's prescribed format must not be obscured by neighboring content. Many firms deliver it as the cover document in the onboarding package precisely to satisfy prominence.

Yes, under the SEC's electronic delivery framework. The standard conditions — notice, access, evidence of delivery, and (in most cases) affirmative consent — apply. Default electronic delivery is permitted under updated SEC guidance subject to specific conditions; consult your operations team and outside counsel on the consent model that fits the firm's clientele.

A natural person, or the legal representative of a natural person, who seeks to receive or receives services primarily for personal, family, or household purposes. A trust where the trustee is a natural person serving a natural-person beneficiary is typically retail; an institutional trustee with institutional purposes is not.

The Commission has not specified pixels or font sizes. In practice, the defensible pattern is a top-level navigation link or a clearly labeled and unambiguously placed footer link, leading to a page with the current Form CRS available as a downloadable or inline document. Burying the link in a sub-footer or behind a "compliance disclosures" hover has been cited as a deficiency.

Form ADV Part 2A is the firm's brochure — a longer document covering the adviser's services, fees, conflicts, and supervisory framework in detail. Form CRS is the two-page summary built for retail investor comparison across firms. The two documents have overlapping content but different audiences and different formats. A retail investor receives Form CRS at the triggering event and Form ADV Part 2A on a separate cadence (initially and on material amendments).

The form requires a yes-or-no answer on whether the firm or its financial professionals have legal or disciplinary history, plus direction to Investor.gov/CRS and BrokerCheck for further detail. A "yes" answer with no other narrative is the prescribed format. Attempts to characterise, minimise, or contextualise disciplinary history within Form CRS itself have been cited as deficiencies; the appropriate place for narrative is the firm's other disclosures (Form ADV Part 2A; BrokerCheck) where the format allows it.

The 30-day amendment clock starts when information in the form becomes materially inaccurate. A material change in fees would generally trigger the clock. The amendment is filed, the website-posted version is updated, and the firm delivers the amendment to retail investors within the applicable delivery window.

Five years for advisers under Rule 204-2(a)(14), with the first two years in an easily accessible place. Three years for broker-dealers under the relevant 17a-3/17a-4 provisions. Many firms align to the longer adviser period across both registrations for operational simplicity.

A typical request asks for: (a) every version of Form CRS the firm has filed; (b) the dates each was filed, posted to the website, and delivered to retail investors; (c) the delivery method and the underlying delivery records for a sample of retail investors; (d) the firm's policies and procedures relating to Form CRS; and (e) evidence of training of the financial professionals who deliver the form. A firm with the five-pillar programme above can produce all of this in under an hour. A firm without typically cannot.

Sedric integrates Form CRS into the broader RIA and wealth-management compliance programme. We help firms move from a brittle manual delivery process to a defensible, examiner-ready Form CRS workflow with versioning, delivery tracking, website-posting synchronisation, and a retention layer that survives a sample-pull request.

Book a working session with our team. We'll walk through your current Form CRS workflow, the delivery log, the website-posting process, and the amendment cadence, and show you the audit export you would hand to an SEC examiner.

Book a demo · For wealth managers and trading firms

Convert your static procedures into active AI controllers that protect your brand 24/7.

.svg)

Scale marketing compliance without slowing down.