Share article on

.svg)

Quick answer: Credit unions follow the NCUA's Truth in Savings rule at 12 CFR Part 707, not the CFPB's Regulation DD, which applies to banks and thrifts. The advertising rule at 12 CFR 707.8 says an ad cannot be misleading, and once it states a rate or offers a bonus, it triggers specific disclosures that must appear clearly and conspicuously.

This guide is for deposit marketing and compliance teams at US credit unions. It covers which rule applies, what counts as a triggering term, and how the rules land on web, email, and social ads.

Credit unions follow NCUA Part 707. Banks and thrifts follow the CFPB's Regulation DD.

Both rules implement the Truth in Savings Act of 1991, but they run on separate tracks. Part 707 is the NCUA's version and it has always governed federally insured credit unions (see 707.1). The CFPB rule, Regulation DD (12 CFR 1030), excludes credit unions by its own terms at 1030.1(c). Under Dodd-Frank, bank and thrift TISA authority moved to the CFPB. NCUA kept Part 707 for credit unions the entire time. If you are copying disclosure language from a bank's playbook, check the citation, because the section numbers differ.

An ad has to be accurate, and any statement of rate or promotional offer pulls in a set of required disclosures. The baseline is truthfulness before you get to the specifics.

Under 707.8(a), an ad cannot be misleading, inaccurate, or misrepresent the account's terms. You cannot call an account "free" or "no cost" if any maintenance or activity fee may apply. You also cannot use the word "profit" to refer to dividends or interest.

When you state a rate, 707.8(b) controls how you say it. The rate has to be stated as the "annual percentage yield" or "APY," using that term. You can abbreviate to "APY" as long as "annual percentage yield" appears at least once. No rate other than the dividend rate may appear, and the dividend rate cannot be more conspicuous than the APY.

Once an ad states an APY, 707.8(c) requires you to disclose several items clearly and conspicuously, as applicable to the account. Skipping one is where most ad findings come from.

A bonus adds its own disclosure set on top of any rate disclosures. A "bonus" is a premium worth more than $10, per 707.2(e).

If your ad offers a bonus, 707.8(d) requires you to disclose the APY (using the term), the time requirement to obtain the bonus, the minimum balance required to obtain it, the minimum opening balance if that is greater, and when the bonus is provided. So a "$150 for opening a checking account" promotion carries deposit-rate style disclosures even when the headline is about cash, not rate.

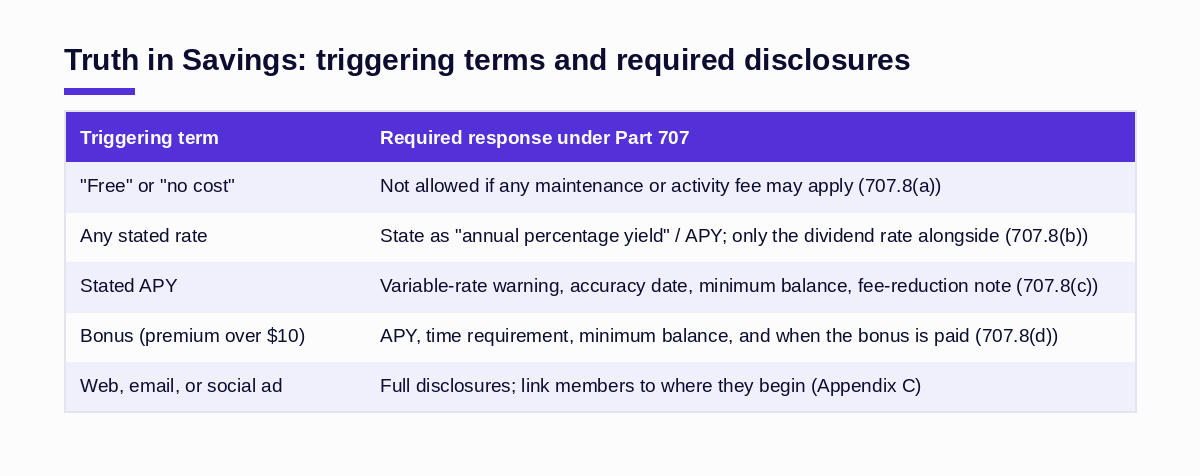

Use this table as a quick screen before an asset goes out. The trigger sits on the left; the required response sits on the right.

| Triggering term or claim | Required response under Part 707 |

|---|---|

| "Free" or "no cost" account | Not allowed if any maintenance or activity fee may apply (707.8(a)). |

| "Profit" for dividends or interest | Not allowed (707.8(a)). |

| Any stated rate | State it as "annual percentage yield"/"APY"; no other rate except the dividend rate, and not more conspicuous than the APY (707.8(b)). |

| Stated APY | Variable-rate warning, accuracy date/period, minimum balance to earn APY (per tier), minimum opening deposit if greater, fee-reduction statement, and term-account items (707.8(c)). |

| Bonus (premium over $10) | APY, time requirement, minimum balance to obtain, minimum opening balance if greater, and when the bonus is provided (707.8(d)). |

Yes. Internet and email ads carry the full disclosures. The broadcast and outdoor exemptions do not cover them.

Part 707 gives some relief to certain media under 707.8(e). Broadcast and electronic media such as TV and radio, outdoor billboards, and telephone-response machines are exempt from certain specific disclosures. Indoor signs are exempt from paragraphs (b), (c), and (d), but if an indoor sign states a rate it must use "APY" and tell members to contact an employee for fees and terms. Newsletters to existing members get the indoor-sign treatment.

Digital ads are treated differently. Under the Official Staff Interpretations in Appendix C, internet and email ads are not covered by the broadcast/electronic-media exemption (Comments 8(e)(1)(i)-1 and -2), so they must carry full disclosures. When an online ad shows a triggering term like an APY or a bonus, it must clearly link the member to where the required disclosures begin (Comment 8(a)-9). An on-premises computer screen counts as an indoor sign, but anything a member can print or keep, such as a brochure or a printout, does not.

Part 707 predates the phrase "social media," so treat your social, email, and web assets as internet advertising governed by the internet and email commentary. That framing keeps you aligned with the rule as written. For the broader picture, see the NCUA advertising rules and our credit union marketing communications compliance guide.

A 707.8 violation is also treated as an advertising violation under NCUA's separate advertising rule. That cross-link raises the stakes on a single missed disclosure.

Part 740.2 states that a violation of 707.8 is also a violation of the Part 740 advertising rules. Examiners work from the NCUA's Part 707 compliance guide when they review deposit advertising, so keeping a clean record of what you published, and why it complied, helps at exam time. UDAAP standards apply to member-facing conduct more broadly, which is worth reviewing alongside your collections and call monitoring practices.

The failure point is rarely the rule itself. It is a live ad that dropped the accuracy date, or a social post that showed an APY without a working link to the disclosures. Sedric pre-screens every marketing asset, including copy, web pages, social, and email, against the credit union's claims library and the applicable Part 707 requirements before it publishes. Each flag ties back to the specific paragraph in 707.8 and is logged, so you have the record ready when an examiner asks.

No. Regulation DD (12 CFR 1030) excludes credit unions at 1030.1(c). Credit unions follow NCUA Part 707, which implements the same Truth in Savings Act for the credit union system.

Only if no maintenance or activity fee may apply to the account. Under 707.8(a), using "free" or "no cost" when any such fee could apply is prohibited.

A bonus is a premium worth more than $10, per 707.2(e). Offers above that amount trigger the bonus disclosures in 707.8(d), including APY, the time and balance requirements, and when the bonus is paid.

No. Broadcast media get relief from certain specific disclosures under 707.8(e), while internet and email ads must carry the full disclosures under the Appendix C commentary.

Convert your static procedures into active AI controllers that protect your brand 24/7.

.svg)

Scale marketing compliance without slowing down.