Share article on

.svg)

Quick answer: Marketing and communications compliance is the discipline of making sure everything a credit union and its partners say to members and prospects is accurate, properly disclosed, and defensible at exam time. For US credit unions the marketing-content rules are NCUA advertising accuracy (12 CFR Part 740) and Truth in Savings (NCUA Part 707), while member communications and collections are judged under the UDAAP standard in the Dodd-Frank Act. This guide maps those rules and shows how to review content and communications at the scale a modern credit union produces them.

There are 4,250 federally insured credit unions in the US serving 145.8 million members and holding $2.48 trillion in assets, according to the NCUA Quarterly Data Summary for Q1 2026. Every ad, rate sheet, disclosure, collections call, and chat message those institutions send is subject to review, and the NCUA looks at consumer financial protection compliance during examinations (2025 Supervisory Priorities, Letter 25-CU-01).

It covers two things: what you publish, and what you say. Published content includes website pages, rate ads, social posts, email, brochures, and in-branch signage, along with the marketing your partners and their partners run in your name. Member interactions include collections and servicing calls, chat, and any member-facing message. Both are held to the same standard: accurate, not misleading, properly disclosed, and consistent with the member's rights.

Three sets of rules do most of the work for marketing content and member communications. The table below is the map; the sections that follow link to a detailed guide for each.

| Area | Rule | What it governs |

|---|---|---|

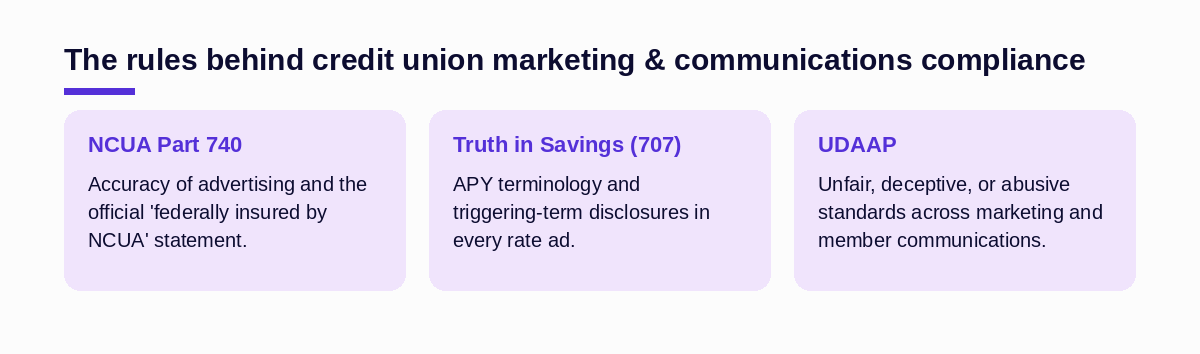

| Advertising & insured status | NCUA 12 CFR Part 740 | Accuracy of advertising and the official insured statement/sign |

| Deposit advertising | NCUA 12 CFR Part 707 (Truth in Savings) | APY terminology, triggering terms, and required disclosures in rate ads |

| Fair treatment | Dodd-Frank 1031 & 1036 (UDAAP); FTC Act Sec. 5 | Unfair, deceptive, or abusive acts across marketing and member communications |

Who examines you for these depends on size. The CFPB supervises credit unions with more than $10 billion in assets for federal consumer financial law, including UDAAP; the NCUA (or a state regulator) supervises those at or below $10 billion (CFPB, institutions subject to supervision). The UDAAP prohibition applies either way; only the examiner changes.

Two rules govern advertising. Part 740 requires that no ad be inaccurate or deceptive and, currently, that most ads carry the official insured statement such as "Federally insured by NCUA" (12 CFR 740.2, 740.5). One item to watch: in December 2025 the NCUA Board proposed removing the official advertising statement requirement as poorly suited to digital media; that proposal is not final, so 740.5 still applies (Federal Register, Dec. 29, 2025).

Part 707, the Truth in Savings rule, governs how you advertise rates: any stated rate must be an annual percentage yield, and terms like a bonus or a minimum balance trigger specific disclosures (12 CFR 707.8). Start with the two detailed guides: NCUA advertising rules and Truth in Savings advertising compliance.

Mostly in collections and servicing. A credit union collecting its own debts is usually a first-party creditor and often outside the FDCPA, but its call conduct is still judged under UDAAP, and the CFPB has said so directly (CFPB Bulletin 2013-07). The conduct rules in Regulation F are the practical benchmark for what to monitor on a call. See UDAAP and collections call monitoring.

Most credit unions review a small percentage of calls and route marketing through a manual sign-off queue. That model made sense when volume was low. It leaves gaps now: the ad that skipped the queue, the collections call in the 98% no one listened to, the partner promotion no one saw before it went out. The rules do not grade on a curve for volume. A misleading rate claim is a violation whether it appeared in the one ad you reviewed or the fifty you did not.

The stakes are set by enforcement in the wider industry. The CFPB ordered Westlake Services and Wilshire Consumer Credit to provide $44.1 million in consumer relief plus a $4.25 million penalty for deceptive collection calls (CFPB). That is a larger institution, but the failure pattern is the one a credit union compliance team manages every day.

A credit union that wants to stay ahead of these rules tends to do five things:

Sedric is an AI platform for communications surveillance and marketing-content compliance. It reviews member communications, marketing assets, and calls and chats, including the marketing your partners and their partners produce, against a credit union's own policies and the applicable rules. It screens content before it goes out and links each flag to the underlying regulation with a logged record for exams. The point is coverage: applying the same standard to everything the credit union and its partners say. You can see how it works at sedric.ai.

No. Credit unions follow NCUA rules, chiefly Part 740 for advertising accuracy and Part 707 for Truth in Savings. Banks follow the CFPB's Regulation DD, which by its terms excludes credit unions.

The CFPB supervises credit unions over $10 billion in assets; the NCUA or a state regulator supervises those at or below $10 billion. The UDAAP standard applies to all of them.

A credit union collecting its own debt is usually outside the FDCPA, but its collection conduct is still reviewed under UDAAP, and the CFPB treats FDCPA-style violations as UDAAP where they apply.

Yes. Marketing-content compliance extends to the member-facing content your partners and their partners create, because the credit union remains accountable for claims made in its name.

Convert your static procedures into active AI controllers that protect your brand 24/7.

.svg)

Scale marketing compliance without slowing down.