Share article on

.svg)

Influencer compliance — also called finfluencer compliance — is the process regulated firms use to ensure that paid endorsements, testimonials, and promotional content created by third-party influencers (or "finfluencers") — whether published on social media, podcasts, video platforms, or newsletters — meet the legal and regulatory standards that apply to the firm's own marketing communications.

The terms "influencer compliance" and "finfluencer compliance" are used interchangeably in financial-services regulation. "Finfluencer" is the regulator-coined shorthand for an influencer who promotes financial products or services, and the term appears explicitly in FCA, ASIC, and FINRA enforcement materials. We use both throughout this guide.

In financial services, that responsibility cuts both ways. The firm is liable for promotions made on its behalf, and the finfluencer can be personally liable if their post falls inside the regulatory perimeter and they lack the licence, authorisation, or approval to communicate it. Both sides face fines, public censure, account takedowns, and — in jurisdictions including the UK and Australia — criminal prosecution.

This guide explains the five regulatory frameworks every regulated firm needs to map influencer and finfluencer marketing against in 2026 (US SEC, US FTC, US FINRA, UK FCA, and EU MiCA), the operational controls those frameworks effectively require, the patterns that keep producing enforcement actions, and how Sedric automates the supervisory layer that turns the rules into something a programme can actually be audited against.

The regulatory environment for financial influencers — finfluencers — has tightened sharply across every major jurisdiction in the last 36 months.

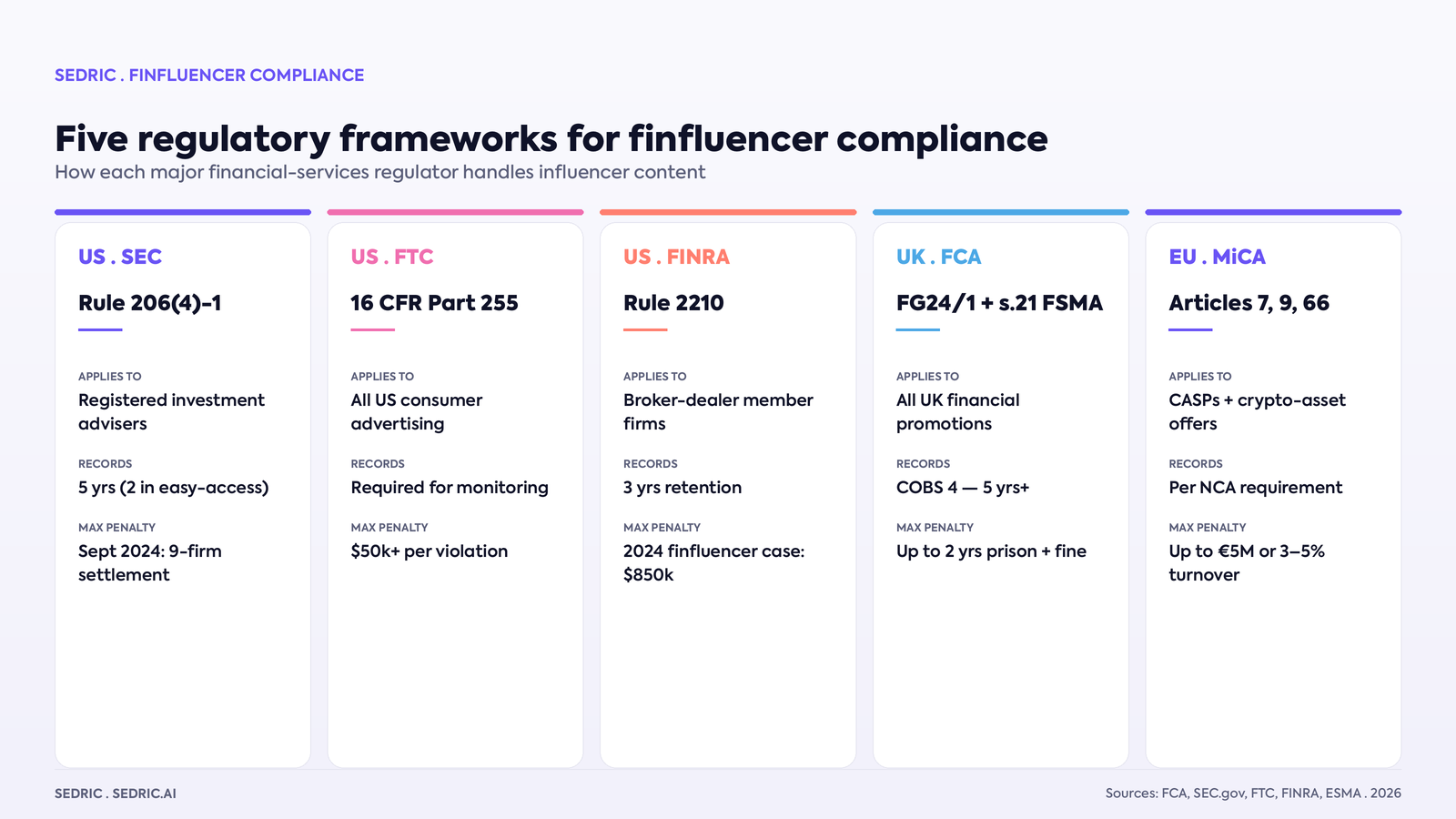

In the United States, the SEC’s Marketing Rule (Rule 206(4)-1 under the Investment Advisers Act of 1940) has been in effect since 4 November 2022 and now allows testimonials and endorsements — including paid finfluencer endorsements — for the first time, subject to mandatory disclosures, written agreements, and supervision. In September 2024, the SEC settled with nine investment advisers for Marketing Rule violations that included unsubstantiated statements and undisclosed endorsements. On 16 December 2025, the SEC's Division of Examinations published a risk alert highlighting persistent failures to provide required disclosures at the point of dissemination across websites, social media, lead-generation firms, and referral networks. The Division of Investment Management updated its Marketing Compliance FAQs on 15 January 2026.

Also in the US, FINRA brought its first enforcement case in 2024 against a broker-dealer's social-media finfluencer programme, fining the firm $850,000 for retail communications that were not fair and balanced and for failures to review, supervise, and retain finfluencer content under Rule 2210.

The FTC finalised revised Endorsement Guides (16 CFR Part 255) on 29 June 2023, effective 26 July 2023, with strengthened standards for "clear and conspicuous" disclosure of material connections — disclosures must be "difficult to miss" and, in interactive media, "unavoidable."

In the United Kingdom, the FCA published its finalised guidance on financial promotions on social media (FG24/1) on 26 March 2024, replacing the 2015 FG15/4 guidance. It then opened a sustained finfluencer-enforcement programme. In May 2024 the FCA charged nine individuals — including several reality-television personalities — in connection with an unauthorised foreign-exchange and contracts-for-difference scheme promoted through Instagram. In October 2024 it issued public alerts against multiple social-media accounts and interviewed a further 20 individuals under caution. In June 2025, the FCA coordinated a week of action with eight other regulators, made three arrests, authorised criminal proceedings against three further individuals, sent seven cease-and-desist letters, issued 50 warning alerts, and triggered more than 650 takedown requests on social platforms. In April 2026, a 17-regulator coordinated sweep secured a guilty plea from former Geordie Shore cast member Aaron Chalmers for illegal financial promotions, alongside criminal proceedings against two further individuals and 120 fresh takedown requests.

In the European Union, Articles 7, 9 and 66 of the Markets in Crypto-Assets Regulation (MiCA) apply to marketing communications published after 30 December 2024. MiCA imposes "fair, clear and not misleading" standards on crypto-asset service providers (CASPs) — including any finfluencer content distributed on their behalf — and requires that marketing communications be identified as such.

In Australia, ASIC’s Information Sheet 269 (INFO 269) has been in force since March 2022, with continuing finfluencer enforcement coordinated with other regulators in 2025 and 2026.

For any regulated firm running, considering, or inheriting a finfluencer programme in 2026, the operative question is no longer "is influencer marketing regulated?" It is "can we evidence, on demand, that every post made on our behalf was reviewed against the relevant rules, disclosed correctly, and retained for the supervisory record?"

The short answer is: both — but in different ways, and the allocation matters when enforcement comes.

The firm is responsible for any promotion made on its behalf, regardless of who pressed publish. That principle is consistent across the SEC, FTC, FINRA, FCA, and MiCA. Where a firm pays, sponsors, gifts, provides affiliate links, supplies talking points, or otherwise materially benefits from a third party's content, the regulator treats the content as the firm's communication and applies the firm's content standards. Lack of approval is not a defence. Inability to retain the content is itself a violation.

The finfluencer is personally responsible whenever their content falls inside the regulatory perimeter. In the US, finfluencers who make recommendations of specific securities can themselves be subject to the federal anti-touting provisions of section 17(b) of the Securities Act of 1933 if they fail to disclose compensation. The FTC also has authority to bring direct enforcement actions against finfluencers for deceptive endorsements. In the UK, communicating a financial promotion in the course of business without authorisation or approval by an authorised person is a criminal offence under section 21 of the Financial Services and Markets Act 2000, punishable by up to two years' imprisonment, an unlimited fine, or both. In Australia, providing financial product advice or "dealing by arranging" without an AFS licence or authorisation is an offence under the Corporations Act 2001.

Standard disclaimers like "this is not financial advice" do not insulate either side. ASIC has stated this explicitly in INFO 269. The FCA and SEC have made functionally the same point in guidance: substance, not labelling, determines whether a communication is a regulated promotion.

The SEC's Marketing Rule, in effect since 4 November 2022, governs how registered investment advisers (RIAs) advertise to clients and prospects, and was the first time testimonials and endorsements were permitted in adviser advertising.

Under the rule, an adviser may use testimonials (statements by current clients) and endorsements (statements by third parties who are not clients, including paid finfluencers) only if all of the following apply:

The Division of Investment Management's January 2026 FAQ updates added clarity on disqualification considerations for compensated endorsements and on the use of model fees when presenting net performance.

The FTC's revised Endorsement Guides, effective since 26 July 2023, apply across all consumer-facing advertising in the United States — including, but not limited to, financial services. They do not preempt or replace SEC or FINRA rules; they sit alongside them.

Key 2023 changes for finfluencer programmes:

For broker-dealer member firms, FINRA Rule 2210 governs all communications with the public — retail communications, correspondence, and institutional communications — including third-party finfluencer content posted on the firm's behalf.

The 2024 enforcement action against a broker-dealer's finfluencer programme — an $850,000 fine — established the supervisory framework FINRA expects:

The FINRA 2026 Annual Regulatory Oversight Report continues to flag communications with the public as a focus area, with finfluencer programmes specifically called out.

The FCA's finalised guidance FG24/1 sits inside the wider section-21 financial promotions regime under the Financial Services and Markets Act 2000. The rules apply to all communications that invite or induce a person to engage in investment activity, regardless of channel or format. Every financial promotion in the UK must be made or approved by an authorised person.

What FG24/1 specifically clarifies for social media and finfluencer content:

Read alongside the FCA's Consumer Duty and the financial-promotions regime, finfluencer compliance in the UK is now one of the FCA's most active enforcement areas.

For crypto-assets, the EU's Markets in Crypto-Assets Regulation (MiCA) applies in full as of 30 December 2024. Three provisions matter most for finfluencer content:

ESMA's MiCA Q&As and the April 2025 final guidelines on market-abuse prevention and detection further extend supervisory expectations around social-media activity, including coordinated finfluencer campaigns that could constitute market manipulation. Firms operating under MiCA should map their finfluencer programmes against the UK FCA's crypto financial-promotion checklist and the MiCA marketing-communication rules — the substantive requirements are aligned even where the procedural mechanics differ.

ASIC's Information Sheet 269, in force since March 2022, applies the existing Corporations Act 2001 regime to social-media finfluencer content. A finfluencer who recommends specific shares, funds, or crypto tokens as "good buys" or "safe long-term holds" is providing financial product advice and must hold an AFS licence or be an authorised representative. Affiliate links and referral codes — particularly where payment depends on followers signing up or transacting — can constitute "dealing by arranging," a separate licensed activity. AFS licensees who engage finfluencers are liable for the finfluencer's misconduct and must conduct due diligence, implement risk-management systems, and monitor the finfluencers they use.

Mapping every regulator's requirements against the realities of running a finfluencer programme produces a six-stage operational framework. The specifics vary by jurisdiction and product, but the structure is consistent across SEC, FTC, FINRA, FCA, MiCA, and ASIC expectations.

Before signing any finfluencer:

Every regulator expects a written agreement that, at minimum:

This is where the operational load lives — and where most finfluencer programmes fail.

A pre-approved script is necessary but not sufficient. The disclosure has to appear in the actual published asset — clearly, prominently, and (for the FTC) unavoidably.

SEC, FINRA, FTC, and FCA frameworks all treat this as a supervisory obligation.

A documented process for what happens when a finfluencer posts content that fails review, repeats prohibited claims, or generates a complaint or alert:

This six-stage framework is the operational layer that turns the regulatory standards into something a finfluencer programme can actually be audited against. The volume problem — every Story, every Reel, every carousel, every podcast read, across every finfluencer, in every jurisdiction — is what makes manual review uneconomical at scale.

The same patterns recur across finfluencer enforcement actions in every jurisdiction.

Inadequate or missing disclosure of material connection. The FTC has brought enforcement actions on this point for over a decade and continues to do so; the 2023 revisions raised the bar further. The SEC's December 2025 risk alert flagged this as the single most common Marketing Rule deficiency.

Cherry-picked or misleading performance claims. Either by the finfluencer or in adviser advertising they appear in. The September 2024 SEC settlement with nine advisers cited untrue or unsubstantiated statements.

Failure to supervise and retain. FINRA's 2024 $850,000 enforcement against a broker-dealer's finfluencer programme rested principally on failures to review, supervise, and retain rather than on the content itself.

Standalone non-compliance. A risk warning that appears in the caption but not in the video itself; a disclosure in the bio link rather than in each individual Story. Every regulator that has addressed the question has rejected this pattern. The FCA's FG24/1 makes the standalone-compliance expectation explicit.

Unauthorised promotion of regulated products. The FCA's finfluencer prosecutions in June 2025 and April 2026 all centred on promoting contracts for difference and other regulated investments without authorisation under section 21 FSMA.

"Dealing by arranging" through affiliate links. ASIC has called this out specifically; finfluencer affiliate programmes that pay on conversion can constitute a financial service in their own right, requiring a separate licence.

Coordinated promotional activity that constitutes market abuse. ESMA's April 2025 MiCA guidelines on market-abuse prevention specifically address coordinated social-media activity around crypto-asset trading. The FCA has investigated similar conduct under the Market Abuse Regulation.

A modern finfluencer programme can produce hundreds of pieces of content per month across multiple formats — video, audio, text — in real time. Manual review can't keep pace with the SEC, FINRA, FCA, and MiCA supervisory expectations laid out above, and the regulators know it. The 2024 FINRA $850,000 enforcement and the December 2025 SEC risk alert both rest, principally, on supervisory and record-keeping failures that scale poorly with humans.

Sedric is the AI compliance platform that closes the gap. The same platform layer covers in-house marketing review, partner and affiliate oversight, and finfluencer programmes — because under every framework above (SEC, FTC, FINRA, FCA, MiCA, ASIC), a finfluencer post is just another financial promotion that has to meet the same standards as everything else.

Pre-publication review. Every piece of finfluencer content — written, audio, or video — is ingested into Sedric and checked against the firm's policy library. The policy library is mapped to the SEC Marketing Rule, FTC Endorsement Guides, FINRA Rule 2210, FCA FG24/1, MiCA Articles 7/9/66, and ASIC INFO 269 out of the box. Firms layer their own product-specific and jurisdiction-specific rules on top.

Multi-format coverage. Sedric processes video, audio (podcasts, sponsored episode reads), and text natively. Disclosure prominence in a 9-second Reel, audibility of a podcast read-out, and on-screen risk warnings in a Story are all assessed by the model — not assumed.

Standalone-compliance checks. Each individual Story, Reel, or post is reviewed in isolation — the way the FCA explicitly requires under FG24/1, and the way the FTC’s standard for "clear and conspicuous" effectively demands — rather than the finfluencer's overall account being given a blanket pass.

Decision logging and retention. Every review decision is timestamped, attributable, and exportable. SEC Marketing Rule materials must be retained for five years (the first two in easily accessible form); FINRA records for three years; FCA COBS 4 for five years or longer. Sedric's retention layer maps to each of those by jurisdiction.

Live monitoring and post-publication oversight. Comment threads, edits, takedowns, and post-publication changes are tracked — so the firm always knows what's been said on its behalf, not just what was approved at the point of publication.

This is the same architecture Sedric uses for partner compliance, where it supervises content distributed by affiliates, AR networks, brokers, and IBs across regulated financial services. It is also the same architecture as marketing compliance review of in-house content. Influencer and finfluencer oversight sits inside the same supervisory system that already runs your marketing and partner content — same policy library, same audit trail, same export, just a different content surface.

For UK FCA-regulated firms, the same Sedric platform handles the wider financial-promotions regime and the Consumer Duty overlay. For US RIAs, it covers the SEC Marketing Rule's testimonial and endorsement disclosure, oversight, and recordkeeping obligations directly. For broker-dealers, it addresses FINRA Rule 2210’s pre-publication review, supervision, and retention requirements. For MiCA-regulated crypto firms, it covers Articles 7, 9, and 66.

Sedric is used by regulated firms across multiple financial-services verticals — banks and issuers, fintechs and neobanks, trading and securities firms, crypto platforms, and debt-collection operations. The platform is the same; the policy library and audit trail adapt to the regulator, the product, and the jurisdiction.

Influencer compliance is the process by which a regulated financial-services firm ensures that paid endorsements, testimonials, and promotional content created by third-party influencers on the firm's behalf meet the legal and regulatory standards applicable to the firm's own marketing communications — including the SEC Marketing Rule and FTC Endorsement Guides in the US, FINRA Rule 2210 for broker-dealers, FCA financial-promotion rules in the UK, MiCA for crypto-asset service providers in the EU, and ASIC INFO 269 in Australia.

Yes — in financial services the terms are used interchangeably. "Finfluencer" is the regulator-coined shorthand for an influencer who promotes financial products or services, and it appears explicitly in FCA, ASIC, and FINRA enforcement language. The compliance obligations are the same regardless of which term is used: a regulated firm must vet, approve, monitor, and retain records of every finfluencer post made on its behalf.

In every major financial-services jurisdiction, yes. A finfluencer whose content falls inside the regulatory perimeter — for example, by promoting a specific regulated investment or providing financial product advice — is subject to the relevant licensing or authorisation regime. In the US, the FTC Act and federal securities laws apply. In the UK, this is section 21 FSMA, and breach is a criminal offence. In Australia, the equivalent is the AFS licensing regime under the Corporations Act 2001. Disclaimers such as "this is not financial advice" do not change the legal analysis.

Yes. Every regulator that has addressed the question — SEC, FTC, FINRA, FCA, ESMA under MiCA, and ASIC — holds the engaging firm responsible for finfluencer content posted on its behalf. Lack of pre-publication review is itself usually a violation. The firm cannot delegate compliance to the finfluencer.

At minimum: a clear and prominent statement of the commercial relationship. For SEC Marketing Rule purposes, the disclosure must also state whether the speaker is a client of the adviser, the fact and material terms of any compensation, and any material conflicts of interest. For FTC purposes, the disclosure must be "difficult to miss" and, in interactive media, "unavoidable" — meaning visible in the actual video, audio, or post, not just in a bio link or buried hashtag.

For SEC-registered investment advisers, Marketing Rule records must be retained for five years from the date the advertisement was last disseminated, with the first two years in an easily accessible place. For FINRA member firms, retail communications retention is generally three years. For FCA-authorised firms, COBS 4 record-keeping obligations apply (generally five years, longer for MiFID business). Retention must include the disclosure and surrounding context, not just the underlying content.

Range varies by regime. FINRA’s first major finfluencer-programme enforcement (2024) was $850,000. The SEC’s September 2024 multi-adviser Marketing Rule settlement involved nine firms and substantial civil penalties. The FTC can impose civil penalties of more than $50,000 per violation under its trade-regulation rule for fake reviews and testimonials. The FCA has secured criminal prosecutions with up to two years' imprisonment available under section 21 FSMA, alongside an unlimited fine. MiCA breaches can trigger administrative fines of up to €5 million or 3–5% of annual turnover depending on the provision.

Yes. The FTC's 2023 revisions explicitly contemplate AI-generated endorsements, and the underlying regulatory standards across all jurisdictions are technology-neutral. A virtual finfluencer making a financial recommendation creates the same regulatory exposure as a human one — both for the operator of the persona and for the engaging firm.

Sedric is an AI compliance platform that ingests finfluencer content across written, audio, and video formats, reviews it against a firm-configurable policy library mapped to each major regulatory framework (SEC, FTC, FINRA, FCA, MiCA, ASIC), flags violations before publication, and retains an audit-ready record of every piece of content and every review decision. The same architecture covers partner and affiliate compliance and marketing compliance review of in-house content — so finfluencer oversight sits inside the supervisory system the firm already runs.

Convert your static procedures into active AI controllers that protect your brand 24/7.

.svg)

Scale marketing compliance without slowing down.