The Fair Debt Collection Practices Act (FDCPA)

is the foundational federal statute governing third-party debt collection in

the United States. Since 1977 it has prohibited specific abusive, deceptive,

or unfair collection practices. In 2026, the FDCPA continues to drive the

largest single share of consumer-protection enforcement and class-action

exposure in the collections industry. This is the operator's checklist —

sixteen items, mapped to the specific FDCPA section and where Reg F overlays

the rule.

What the FDCPA Covers

The FDCPA applies to third-party debt collectors — agencies, debt buyers,

and attorneys collecting on behalf of others — when collecting consumer debt

(debt for personal, family, or household purposes). First-party creditors

collecting their own debt are not directly covered by the FDCPA but face

parallel obligations under state UDAP statutes and CFPB UDAAP authority.

The statute's six substantive areas:

Communications with consumers and third parties — when,

how, and with whom collectors can communicate (§§ 1692c, 1692b).

Harassment or abuse — prohibitions on threats, profane

language, repeated calls, and similar conduct (§ 1692d).

False or misleading representations — bans on false

statements about the debt, the collector, or legal action (§ 1692e).

Unfair practices — prohibitions on collecting amounts

not authorised, using post-dated checks improperly, or non-authorised

fees (§ 1692f).

Validation of debts — the consumer's right to dispute

and the collector's obligation to verify (§ 1692g).

Civil liability — actual damages plus statutory

penalties to $1,000 per violation, plus attorneys' fees (§ 1692k).

The CFPB's 2021 Regulation F adds operational specificity — call

frequency, communications media, validation notice format. Modern FDCPA

compliance means operating to both the statute and the regulation.

Why FDCPA Compliance Matters in 2026

Three forces have raised the operational bar:

The CFPB's supervisory cadence has accelerated. The

Bureau's 2024-2025 examination programme has focused heavily on

debt-collection, with particular emphasis on validation notice compliance,

call-frequency rules, and credit-reporting accuracy.

State AGs are filing significant actions. Multi-million-dollar

settlements have become routine. State-level cures often impose monitoring

requirements that exceed federal baseline.

Class-action exposure compounds. A single mishandled call

surfacing in discovery can ground a class action with statutory damages

multiplied across the affected population.

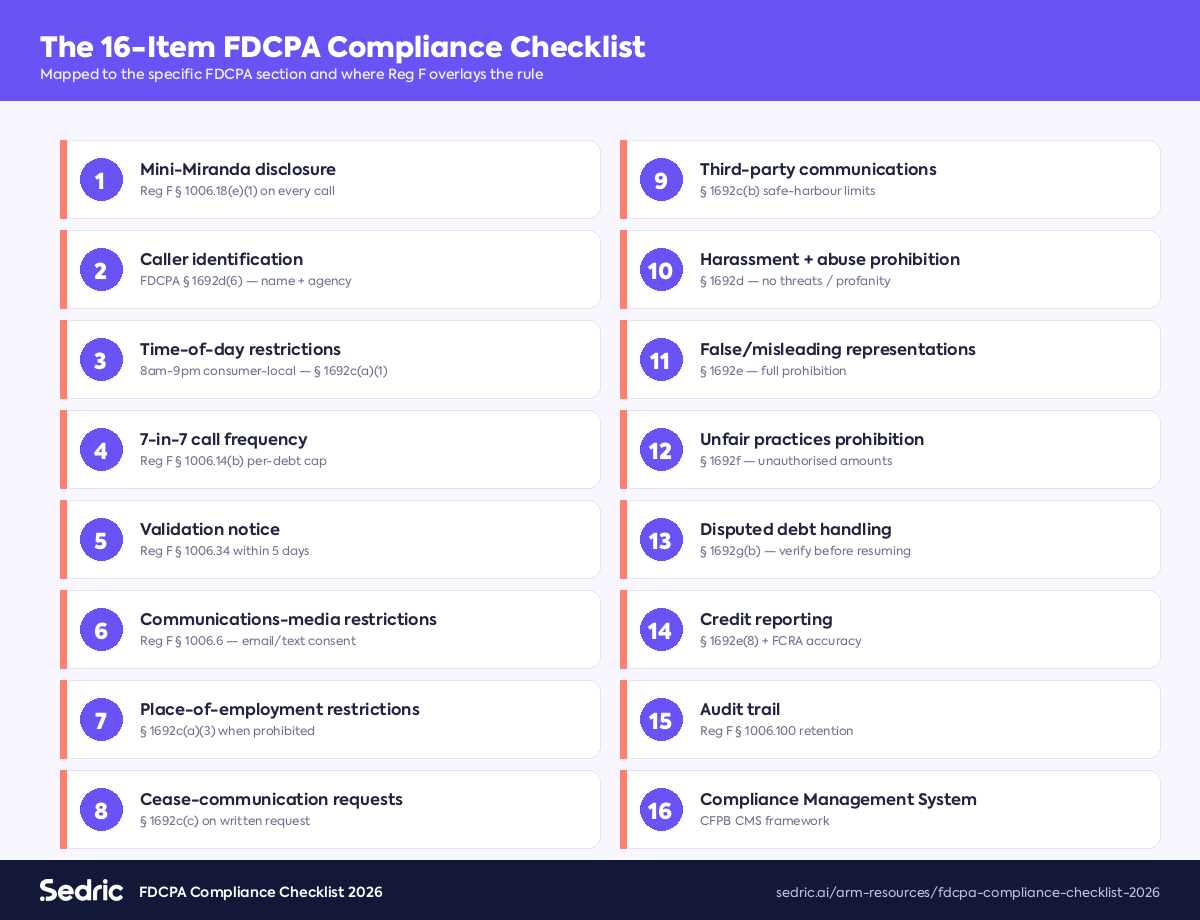

The 16-Item FDCPA Compliance Checklist

Mini-Miranda disclosure. Every collection call opens

with the prescribed disclosure: "This is an attempt to collect a debt and

any information obtained will be used for that purpose." Reg F § 1006.18(e)(1).

Caller identification. The collector identifies themselves

and their agency by name. § 1692d(6).

Time-of-day restrictions. No calls before 8 a.m. or after

9 p.m. consumer-local time, unless the consumer consents otherwise.

§ 1692c(a)(1).

7-in-7 call frequency. Reg F caps collection calls at 7

per debt per 7 days, with a 7-day quiet period after talking with the

consumer. § 1006.14(b).

Validation notice. Within 5 days of the initial communication,

provide the Reg F-specified validation notice with itemisation, current

balance, account information, and consumer-protection statements. § 1006.34.

Communications-media restrictions. Email and text only

with consumer consent (or via the limited-content message safe harbour).

§ 1006.6.

Place-of-employment restrictions. If the consumer or

employer indicates that the employer prohibits such communication, the

collector must stop calling there. § 1692c(a)(3).

Cease-communication requests. Once a consumer requests

in writing that the collector cease communication, the collector must

stop except for specified safe-harbour purposes. § 1692c(c).

Third-party communications. Communications with anyone

other than the consumer (spouse, attorney, guarantor, etc.) are restricted

to specific safe-harbour scenarios. § 1692c(b).

Harassment and abuse prohibition. No threats, profane

language, calls intended to annoy or harass, or repeated calls. § 1692d.

False or misleading representations. No false statements

about amount owed, legal action threatened, collector's identity, or

consumer-rights implications. § 1692e.

Unfair practices prohibition. No collection of unauthorised

amounts, no post-dated checks misused, no deposit threats. § 1692f.

Disputed debt handling. If the consumer disputes the debt

within the validation period, cease collection until the collector verifies

the debt and provides verification to the consumer. § 1692g(b).

Credit reporting. Don't report disputed debt without

noting the dispute; don't report inaccurate information. § 1692e(8); FCRA

overlay.

Audit trail. Every call, message, validation notice,

and consumer interaction logged with timestamp, agent ID, and disposition.

Reg F § 1006.100 retention requirements.

Compliance Management System. Documented policies,

training, monitoring, corrective action, and board-level oversight,

aligned to CFPB CMS expectations.

Common FDCPA Violations That Trigger Enforcement

Failure to deliver a compliant validation notice within 5 days.

Calls exceeding the 7-in-7 frequency cap, particularly across multiple

debts attributed to the same consumer.

Texts or emails to consumers who never opted in.

Mini-Miranda omission on subsequent calls (it's required on each

collection communication, not just the first).

Place-of-employment calls after the employer's prohibition is known.

Third-party disclosure of debt status (most commonly to family members

or co-workers in voicemail or call-back contexts).

Threats of legal action that the collector has no intention of taking.

Misrepresentation of the consumer's rights, particularly around credit

reporting and dispute consequences.

How Sedric Helps

Sedric monitors 100% of collection calls and messaging in real time,

scoring each interaction against the full FDCPA + Reg F rulebook plus the

firm's policy library. The agent-assist surface whispers required disclosures

(mini-Miranda, validation, time-of-day) to the agent at the right moment.

Every flag is mapped to the specific FDCPA section or Reg F provision it

engages, and every override is logged with reasoning — the exact audit

trail a CFPB examiner expects.

FAQ

Does the FDCPA cover first-party creditors collecting their own debt?

Not directly. First-party creditors face parallel obligations under CFPB

UDAAP and state UDAP statutes; many also adhere to FDCPA standards voluntarily

to maintain consistency across the collection lifecycle.

What's the statutory penalty for an FDCPA violation?

Up to $1,000 per consumer in statutory damages, plus actual damages and

attorneys' fees. Class actions can multiply this dramatically.

How does Reg F change FDCPA compliance?

Reg F operationalises the FDCPA — adding the 7-in-7 rule, validation

notice format, communications-media rules, and recordkeeping. Modern

compliance means satisfying both statute and regulation simultaneously.

Are voicemails communications under the FDCPA?

Yes. A voicemail counts as a communication. The limited-content message

safe harbour in Reg F § 1006.2(j) provides specific format requirements

that allow a voicemail without triggering third-party disclosure liability.

How long do I need to retain collection records?

Reg F § 1006.100 requires 3 years from the last collection activity for

most records, with longer retention for certain recordings and validation

notice evidence.

The Bottom Line

FDCPA compliance in 2026 is not a static checklist exercise — it's an

operational discipline that must run live, across every collection

conversation, every channel, every state. The firms that handle it well

have real-time monitoring with rule-mapped flagging, agent-assist that

prevents violations before they occur, and an audit trail that survives

both regulator examination and class-action discovery.

See Sedric in action

Sedric is the AI compliance platform for regulated marketing and communications. Every flag is mapped to the specific rulebook provision, every override is logged with reasoning, and the audit trail is the format regulators expect on first request. Book a 30-minute demo and we will walk through your specific compliance footprint.

.svg)

![Featured image for 'FDCPA Compliance Checklist 2026' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a15f18a7f2f5ce264082ae7_6a15f18512b4bfdc437d7d92_featured-rebrand-fdcpa-compliance-checklist-2026.png)

.svg)

.avif)

![Featured image for 'AI in Debt Collection Compliance: How Agent-Assist Changes the Operating Model' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a15f17925f21ab4460678fd_6a15f176bd2ec6cdff9602e1_featured-rebrand-ai-debt-collection-compliance-2026.png)

![Featured image for 'State Debt Collection Laws 2026: A Practitioner's Map' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a15f17ebc29bfe311dd0d28_6a15f17b18c1990398b7991f_featured-rebrand-state-debt-collection-laws-2026-practitioners-map.png)

![Featured image for 'CFPB Reg F: The 2026 Operator's Guide' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a15f184b9e16b2074c63303_6a15f180de817f5765d9678b_featured-rebrand-cfpb-reg-f-2026-operators-guide.png)