Sedric Team

Communications

Share article on

.svg)

![Featured image for 'AI in Debt Collection Compliance: How Agent-Assist Changes the Operating Model' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a15f17925f21ab4460678fd_6a15f176bd2ec6cdff9602e1_featured-rebrand-ai-debt-collection-compliance-2026.png)

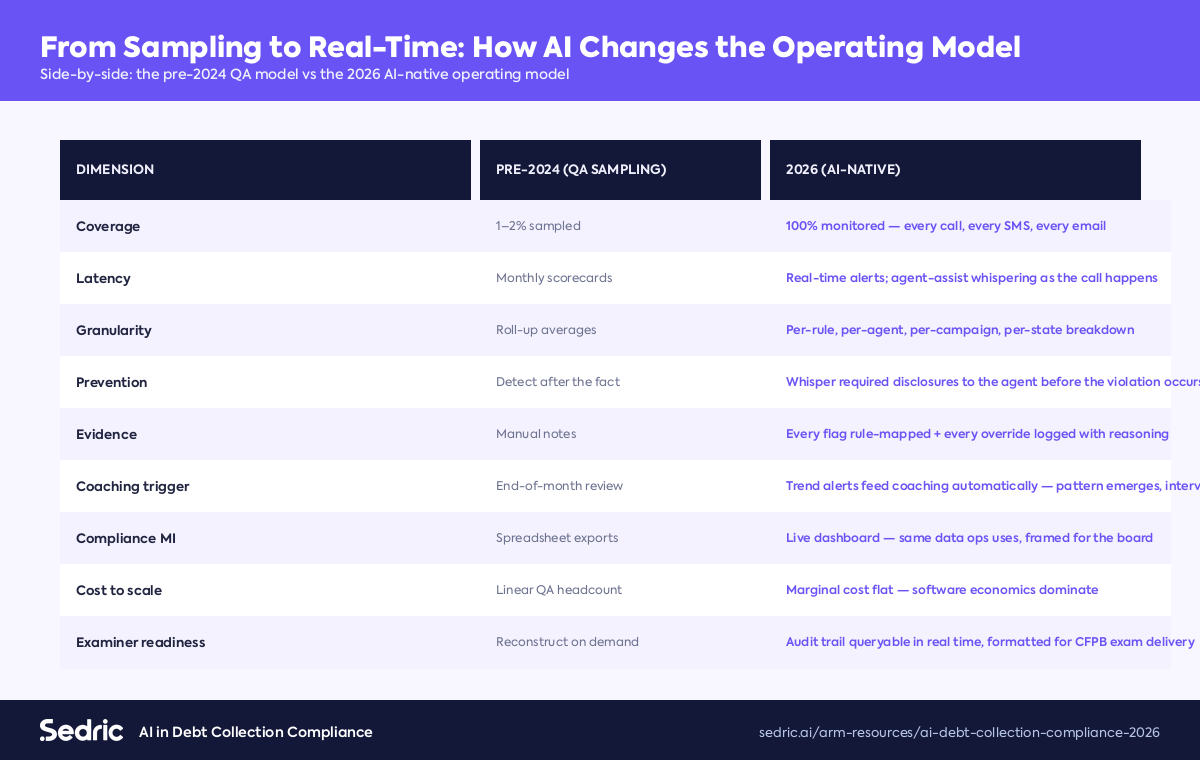

AI-native compliance monitoring has moved debt-collection oversight from sampling-and-bottlenecks to continuous-and- real-time in 2026. Where the operating model used to mean a QA team sampling 1-2% of calls and producing monthly scorecards, modern collection operations monitor 100% of customer-facing conversations in real time, score every interaction against the firm's policy library and the regulatory rulebook, and surface required disclosures through agent-assist before the agent even needs to remember them. This is how that change works, what it costs, where it's been deployed, and how Sedric fits.

For three decades, debt-collection compliance worked like this:

The model worked at scale up to a point. It failed under three pressures that emerged in the 2020s: regulatory rule specificity (Reg F made violations rule-mapped and testable), consumer-protection litigation volume (plaintiffs' bar found that even one mishandled call could ground a class), and the rising cost of compliance headcount (QA teams scaled linearly with call volume, but the regulatory bar kept rising).

By 2026, sampling-based compliance is no longer defensible at any meaningful operational scale.

The new model has five components:

Every call scored live against the rule library. Mini-Miranda absent? Flagged at second 20. Time-of-day violation? Pre-flagged before dial. Place-of-employment restriction? Flagged if call destination matches prohibited workplace.

Validation notice generated from account data, formatted to § 1006.34 specifications, delivered within 5 days, with delivery and consumer-response tracking. The most-cited Reg F finding — validation defects — engineered out of the operating model.

Pre-call enforcement of the 7-in-7 rule, time-of-day windows, and cease-and-desist lists. The platform integrates with the dialler to suppress calls that would violate the rule rather than relying on agent discipline.

Email and text only when consent is on file or limited-content safe harbour conditions are met. Opt-outs honoured automatically across channels.

100% of completed calls re-scored post-call, with deeper analysis than real-time allows. Trending and root-cause across agent, campaign, debt type, and consumer segment.

Inbound complaints automatically linked to the underlying call evidence. Root-cause patterns surfaced from the call transcripts themselves — not from manual reconstruction after the fact.

State-specific calling-hour windows, disclosure templates, and communication restrictions applied automatically based on the consumer's state. The Massachusetts-vs-Texas operational difference handled at the infrastructure layer.

Sedric is built on the industry's first compliance-dedicated large language model — a model trained on financial-services regulatory language and continuously evaluated against new enforcement themes. The platform sits across the collection workflow: real-time call scoring, agent-assist whispering, dialler-layer Reg F enforcement, validation notice workflow, 100% post-call QA, complaint root-cause, and state-law overlay routing.

Every flag carries a rationale tied to the specific FDCPA section or Reg F provision; every override is logged with reasoning. The audit trail is the exact format a CFPB examiner expects on first request. Sedric customers include national creditors, bank-owned collection operations, specialty consumer-credit firms, and large third-party agencies.

No, and the CFPB is explicit on this. AI accelerates and improves compliance, but human-in-the-loop oversight, qualified-person approval, named accountabilities, and override discipline remain non-negotiable.

Coverage from 1-2% to 100%; cycle time from monthly to real-time; QA headcount typically reduced 30-60% while compliance posture improves.

Two-party-consent states require disclosure that the call is recorded and monitored. Modern platforms include this in the agent script. The underlying recording and AI analysis are otherwise compatible with two-party-consent regimes.

Yes. Open API integration with Five9, NICE, Genesys, Aspect, and most CRM platforms is supported. The platform sits alongside existing infrastructure rather than replacing it.

60-90 days to first production use for most operators. Dialler integration is typically the longest pole; once that's complete, the rest follows quickly.

AI-native debt-collection compliance is the new operational baseline. Sampling-based oversight cannot meet the regulatory bar in 2026, cannot defend against class-action discovery, and cannot scale with the rising cost of compliance headcount. The firms that handle this well operate to 100% real-time monitoring, with rule-mapped flagging, agent-assist prevention, and an audit trail that survives both CFPB examination and plaintiff discovery on first request.

Sedric monitors 100% of your collection conversations in real time, scores each against the FDCPA + Reg F + your state-law overlay, and produces the audit trail the CFPB expects. Book a 30-minute demo — we'll review your own calls, map findings to the specific rule, and show what 100% coverage looks like.

Convert your static procedures into active AI controllers that protect your brand 24/7.

.svg)

.avif)

You’ll be able to see a full demo of marketing and communications compliance with your brand.

![Featured image for 'State Debt Collection Laws 2026: A Practitioner's Map' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a15f17ebc29bfe311dd0d28_6a15f17b18c1990398b7991f_featured-rebrand-state-debt-collection-laws-2026-practitioners-map.png)

![Featured image for 'CFPB Reg F: The 2026 Operator's Guide' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a15f184b9e16b2074c63303_6a15f180de817f5765d9678b_featured-rebrand-cfpb-reg-f-2026-operators-guide.png)

![Featured image for 'FDCPA Compliance Checklist 2026' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a15f18a7f2f5ce264082ae7_6a15f18512b4bfdc437d7d92_featured-rebrand-fdcpa-compliance-checklist-2026.png)