Debt collection compliance software is the

operational system that lets a creditor, debt buyer, or third-party collection

agency monitor every customer-facing conversation — calls, chat, email,

texts, dialler campaigns — for compliance with the FDCPA, CFPB Reg F, and the

patchwork of state debt-collection laws, in real time, at 100% coverage. In

2026 the category is no longer optional for any operator with material call

volume: the CFPB's 2024-2025 supervisory cadence, the state attorneys-general

sweeps, and the rise of consumer-protection class actions have made retrospective

sampling untenable. This guide sets out what the software should do, build vs

buy, evaluation criteria, vendor archetypes, and where Sedric fits as the

AI-native option.

Why Debt Collection Compliance Software Matters in 2026

The economics of debt-collection compliance have shifted. A decade ago, a

QA team sampled 1-2% of calls, generated monthly scorecards, and called it

oversight. That model fails 2026 supervision for three reasons:

CFPB Reg F changed the game. Since November 2021, Reg F

codifies prescriptive rules on call frequency (the 7-in-7 rule), validation

notice content, communications media restrictions, and recordkeeping.

Compliance is rule-mapped and testable — exactly what Reg F examiners

ask for.

State AG enforcement is escalating. California, New York,

Massachusetts, Illinois, Texas, Washington — multiple state AGs have brought

significant debt-collection actions in 2024-2025. Each state's rules differ;

operating without state-aware compliance creates exposure across the

collection-jurisdiction footprint.

Consumer plaintiffs' bar has gone digital. Class-action

firms now use call-recording transcripts as evidence. A single mishandled

call surfacing in discovery can cascade into a class.

The operational answer is software that monitors 100% of communications

in real time, flags violations against rule, captures evidence of the firm's

corrective action, and produces the artefact base supervisors expect.

What Debt Collection Compliance Software Should Do

A 2026-grade platform covers, at minimum, the following capabilities:

Real-time call monitoring. 100% of outbound and inbound

collection calls captured, transcribed, and scored against FDCPA / Reg F /

state-law rule library — live, while the agent is still on the line.

Agent-assist surfacing. The platform whispers the

required disclosure (mini-Miranda, debt validation, call-frequency caution)

to the agent at the right moment, reducing accidental violations.

Post-call QA at scale. Automated 100% sample of completed

calls, scored against the firm's policy library and the rulebook.

Communications-media coverage. Calls, SMS, email,

chat, and any consumer-facing portal interaction — all monitored, all

audit-trailed.

Dialler integration. Pre-call enforcement of Reg F

call-frequency limits, time-of-day rules, do-not-call lists, and consumer

opt-outs.

Validation notice management. Workflow to generate, send,

and track the Reg F validation notice within the 5-day window, with consumer

response handling.

Complaint root-cause analysis. Complaints by AR, by

campaign, by agent — root-cause patterns surfaced from the underlying call

data.

Recordkeeping. Every call, every notice, every consumer

interaction retained for the rule-required retention period (typically 3

years under Reg F § 1006.100), in an FCRA-aligned audit-trail format.

State-law overlay. Per-state license tracking, disclosure

mandates, communication restrictions, calling-hour rules, debt-validation

deadlines — all encoded as a rule library.

A platform covering all ten is rare. Most buyers end up combining a

purpose-built compliance platform (capabilities 1-4, 8-10) with their

existing dialler / CRM (5-7).

Build vs Buy

In 2026 the build path for collections compliance is closed for any

operator not running a multi-hundred-million-dollar book. The reasons:

The AI capability is hard. Speech-to-text plus

compliance-aware natural-language processing requires a fine-tuned model

stack, regulator-aware language models, and continuous evaluation against

new enforcement themes. Not a build-it-yourself project.

The rule library is wide. FDCPA, Reg F, the 50-state

patchwork, evolving CFPB guidance, FTC Holder Rule, TCPA, GLBA, and the

FCRA all overlap on debt-collection conduct. Encoding the rulebook

correctly is a vendor specialty.

Volume drives economics. Vendors operating across many

clients realise economies of scale (model improvement, regulatory updates,

shared compliance intelligence) that no single firm can match in-house.

The decision is rarely whether to buy — it's which vendor archetype to buy.

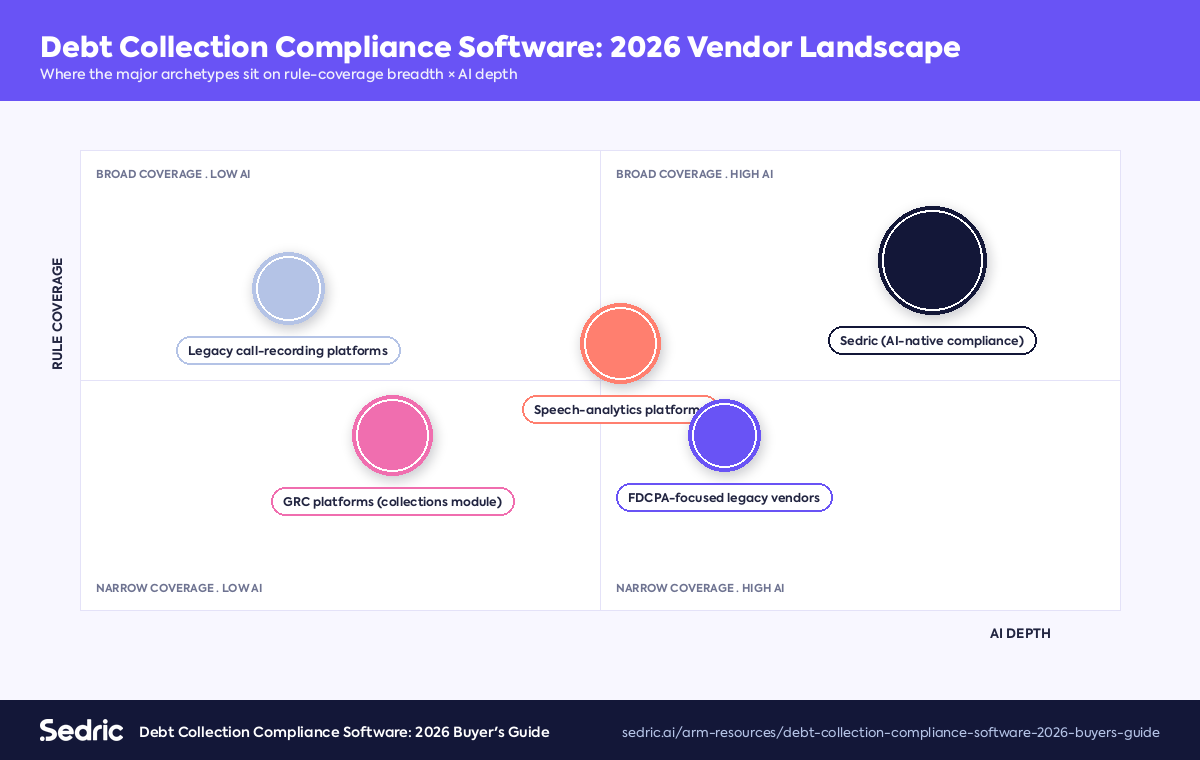

Vendor Archetypes in the Category

Legacy call-recording platforms. Strong on capture +

retention. Weaker on real-time scoring, AI-native rule mapping, and rule

library breadth.

Speech-analytics platforms. Strong on post-call QA at

scale. Variable on real-time, on Reg F-specific rule encoding, and on

state-law overlay.

GRC platforms with debt-collection modules. Strong on

policy management and case workflow. Weaker on the operational call

monitoring that is the heart of the discipline.

AI-native compliance platforms. Strong on real-time

scoring, rule-mapped flags, agent-assist, and continuous improvement.

Sedric sits in this category — built on the industry's first

compliance-dedicated LLM.

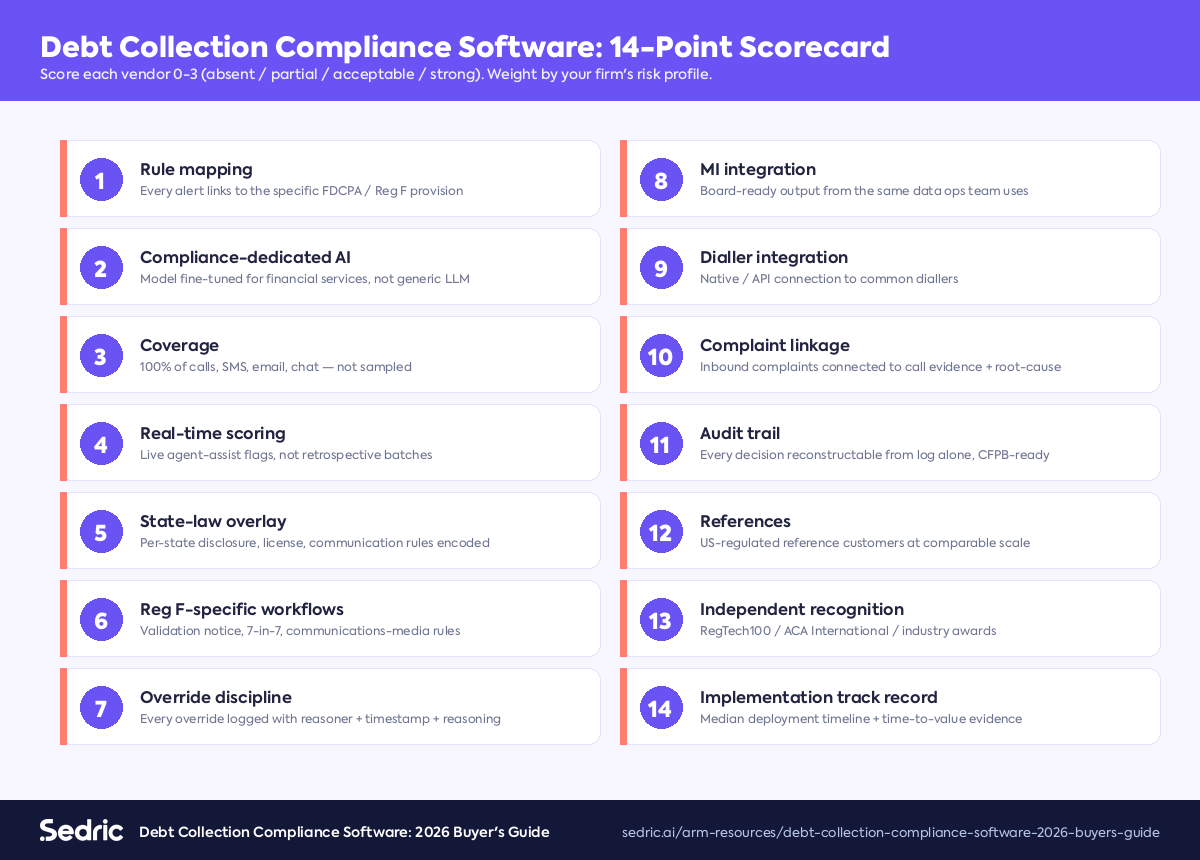

The 14-Point Evaluation Scorecard

Score each vendor 0-3 (absent / partial / acceptable / strong). Weight by

your firm's specific risk profile.

Rule mapping. Does every alert link to the specific

FDCPA / Reg F / state-law provision it engages?

Compliance-dedicated AI. Models fine-tuned for financial

services compliance, or general-purpose LLM with prompt engineering?

Coverage. 100% of calls, SMS, email, and chat — or

sampled?

Real-time scoring. Live flags surfaced to the agent, or

batch-processed retrospectively?

State-law overlay. Per-state disclosure, license, and

communication restrictions encoded — or generic federal-only logic?

Override discipline. Every alert override logged with

reasoner identity, timestamp, and reasoning?

MI integration. Board-ready outputs from the same data

the operational team uses?

Dialler integration. Native or API-based connection

to common diallers (Five9, NICE, Genesys, Aspect, etc.)?

Complaint linkage. Inbound complaints connected to

underlying call evidence, with root-cause analysis?

Audit trail. Every decision reconstructable from log

alone, ready for CFPB exam delivery?

References. UK-regulated and US-regulated reference

customers at comparable scale, in your sector (creditor / debt buyer /

agency / first-party servicer)?

Independent recognition. RegTech100, ACA International,

or comparable industry recognition? Backed by reputable institutional

investors?

Implementation track record. Median deployment timeline,

references that confirm time-to-value?

How Sedric Helps

Sedric is built on the industry's first compliance-dedicated large

language model. The platform monitors 100% of collection-call conversations

in real time, scoring each call against the firm's policy library, the FDCPA,

CFPB Reg F, and the relevant state-law overlays. Every alert is rule-mapped;

every override is logged with reasoning. The agent-assist surface whispers

required disclosures, called-frequency cautions, and consumer-rights language

to the agent at the right moment.

Sedric customers include large-scale creditors, debt buyers, banks, and

specialty consumer-credit firms. The platform sits alongside the firm's

existing dialler, CRM, and complaints system — integrating through an

open API — rather than replacing them. The use-case Sedric is uniquely

well-suited to: monitoring what the collection floor is actually saying,

in real time, at 100% coverage, with rule-mapped output the firm can

defend in a CFPB examination.

FAQ

Is debt collection compliance software required by law?

No federal law mandates a specific software. The CFPB and state regulators

require that creditors and collection agencies maintain a Compliance

Management System adequate to the firm's risk profile. For any operator

above modest call volume, software is the only practical way to meet that

standard.

What's the difference between FDCPA software and Reg F software?

FDCPA is the statutory framework (1977). Reg F is the CFPB's implementing

regulation, in force since November 2021, that adds prescriptive operational

rules on call frequency, validation notice, communications media, and

recordkeeping. Modern software covers both.

How much does this typically cost?

Pricing varies widely. Per-seat models, per-call models, and platform

subscriptions are all common. Mid-market collection agencies typically

budget in the low-six-figure range annually; large creditors with high

call volume often invest seven figures.

How long does implementation take?

For most operators, 60-90 days to first production use. Dialler integration

is typically the longest pole.

What does the CFPB look for in a debt-collection software review?

Evidence that the firm's monitoring actually catches violations, that

the firm's response to flagged violations is timely, that the audit trail

is complete, and that the firm's Compliance Management System uses the

software's outputs to improve operations.

The Bottom Line

Debt collection compliance software is no longer a nice-to-have — it's

the operational backbone of a defensible compliance management system in

2026. The firms that handle it well have real-time visibility into 100% of

their customer-facing conversations, rule-mapped flagging tied to the

specific FDCPA / Reg F / state-law provision, and an audit trail that

survives CFPB examination on first request. Sedric is built for the firms

that intend to operate at that bar.

See Sedric in Action

Sedric's debt-collection compliance platform monitors 100% of your

collection calls, SMS, email, and chat conversations in real time, scores

each against the FDCPA, Reg F, and your state-law overlay, and produces

the audit trail the CFPB expects. Book a 30-minute

demo — we'll review a sample of your own calls, map findings to the

specific rule, and show what 100% coverage looks like end-to-end.

.svg)

![Featured image for 'Debt Collection Compliance Software: 2026 Buyer's Guide' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a15f190937c9f9185634d10_6a15f18c3e26f0692a237df5_featured-rebrand-debt-collection-compliance-software-2026-buyers-guide.png)

.svg)

.avif)

![Featured image for 'AI in Debt Collection Compliance: How Agent-Assist Changes the Operating Model' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a15f17925f21ab4460678fd_6a15f176bd2ec6cdff9602e1_featured-rebrand-ai-debt-collection-compliance-2026.png)

![Featured image for 'State Debt Collection Laws 2026: A Practitioner's Map' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a15f17ebc29bfe311dd0d28_6a15f17b18c1990398b7991f_featured-rebrand-state-debt-collection-laws-2026-practitioners-map.png)

![Featured image for 'CFPB Reg F: The 2026 Operator's Guide' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a15f184b9e16b2074c63303_6a15f180de817f5765d9678b_featured-rebrand-cfpb-reg-f-2026-operators-guide.png)