Share article on

.svg)

![Featured image for 'Appointed Representative Management Software: A 2026 Buyer's Guide' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a0b81b9a37b1eb99f276b09_6a0b81b7a37b1eb99f276a4c_featured-rebrand-appointed-representative-management-software.png)

TL;DR — The AR regime in 2026 cannot be operated on spreadsheets at scale. Principal firms with material AR books are sourcing dedicated appointed representative management (ARM) software to handle register management, attestation workflow, financial promotion approval, communications monitoring, MI and complaint integration. This buyer's guide sets out what the category should do, the build-versus-buy question, integration considerations, evaluation criteria, and where Sedric fits as the AI-native option.

Before PS22/11, AR oversight at most principals was a SharePoint folder and a spreadsheet. The annual return, the F&P file, the financial promotion approvals and the supervisory visit log were managed manually. The regulator was less data-hungry and the operational burden was modest.

That model has been overrun. PS22/11 introduced mandatory annual self-assessment, expanded notification triggers, AR-level revenue and complaints reporting, and explicit due diligence and oversight requirements. The 2022 Dear CEO letter, subsequent supervisory updates, and a steady cadence of section 166 reviews have moved the bar from "evidence the activity" to "evidence the operation of the activity, in real time, against the population." A 100-AR network principal cannot do that on spreadsheets without producing the kind of inconsistency a skilled person will find inside a week.

The result is a real category. ARM software is now a buyer's market with several vendor archetypes:

The well-organised principal builds an architecture that covers each capability — see the build vs buy section below.

A practitioner's working list of the capabilities a 2026 ARM platform should cover:

A platform that covers all ten is rare. The buyer's question is which capabilities are best served by which vendor, and what the integration story is between them.

The AR register is the data foundation that every other capability depends on. A defensible register in 2026:

The register is the document the FCA will ask for first in any supervisory engagement. If the register is in five places, the supervisory engagement is harder than it needs to be. See FCA appointed representative regime 2026 for the regulatory expectation set the register is supporting.

PS22/11 introduced the mandatory annual self-assessment. A platform that does the self-assessment well will:

The platform should be the single self-assessment system of record. Word documents stitched together from spreadsheets and SharePoint folders are the failure mode every skilled person identifies.

Every AR financial promotion is a principal financial promotion. The s.21 FSMA and rulebook compliance burden sits at the principal, and the approval queue is the operational point of control.

What good looks like:

For the regulatory framework the approval queue is implementing, see financial promotions rules 2026 and the COBS 4 guide. The approval queue is the operational application of those rules through the AR chain.

This is the capability where the category has matured most over the last 18 months and where most legacy ARM platforms are weakest.

The problem the principal is solving: an AR's customer conversations — calls, chat, email, social media activity by AR staff, customer-facing video — are conversations the principal is regulatorily responsible for, but historically the principal had no operational way of seeing them. Communications monitoring closes that gap.

A 2026 capability looks like:

This is the capability that lets a principal scale an AR network without scaling its supervisory headcount. It is also the capability skilled persons find missing on the typical AR-oversight s.166. See our overview of the section 166 process for context.

The board has to see — and challenge — the AR oversight position. A 2026 dashboard should produce, in real time:

The dashboard should generate a board pack with one click — the same data the AR oversight team uses operationally, framed for governance challenge. See our principal firm oversight obligations deep dive for what the governance challenge should look like.

DISP 1 requires the principal's complaints arrangements to capture AR-distributed business. A 2026 ARM platform supports that with:

The complaints function and the AR oversight function should see the same data on the same dashboard.

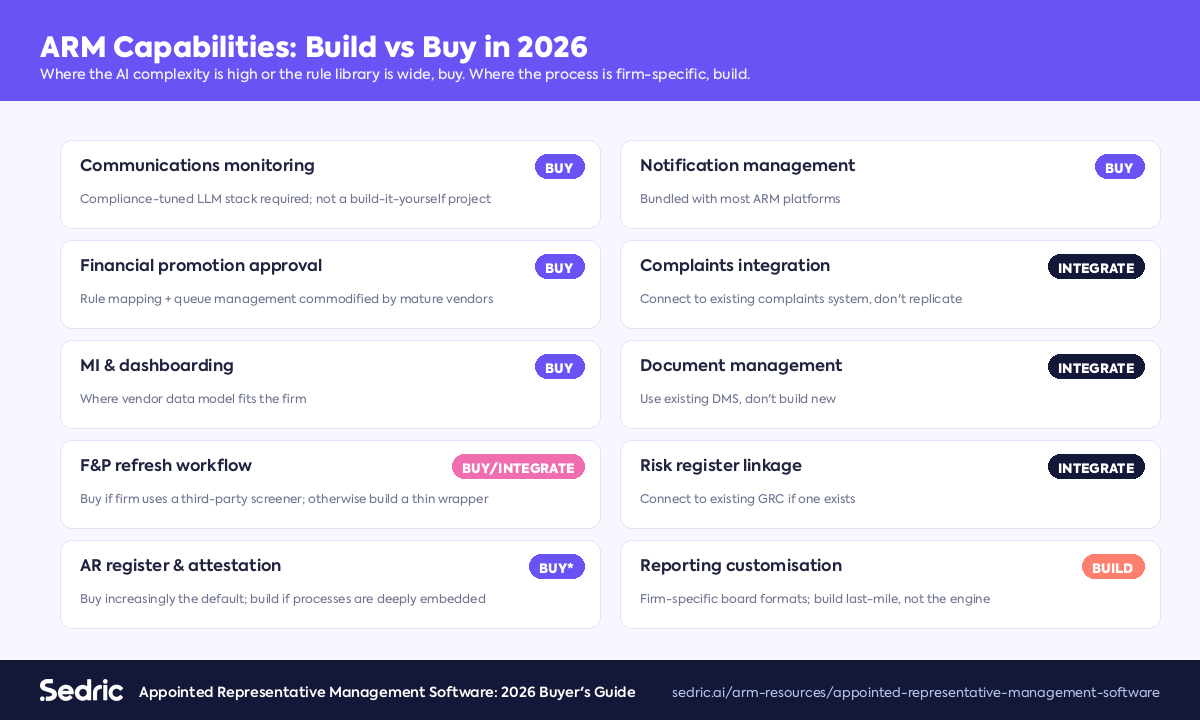

The "build vs buy" question for ARM software in 2026 is rarely binary. Most network principals end up with a mixed architecture — buying for the capabilities where the regulatory complexity is high or the AI is hard, and building for the capabilities that are firm-specific.

Generally:

The build path that has fallen out of favour is "build a comms monitoring system in-house." The compliance-tuned LLM stack required is no longer a reasonable in-house build for any firm whose core competency is regulated activity rather than data science.

ARM software does not live alone. It connects to:

The integration story is the buying decision as much as the feature list. A vendor with five out of ten capabilities, deep integrations and an open API beats a vendor with eight out of ten capabilities and a closed environment.

The two integration risks to evaluate:

When evaluating an ARM vendor:

Score each capability from 0 to 3 (absent / partial / acceptable / strong). Apply weight by your specific risk profile. A network principal in retail advice will weight communications monitoring and FinProm approval more heavily than will an institutional broker-dealer with a small AR book.

Sedric is the AI-native option in the category. Built on the industry's first compliance-dedicated LLM, the platform monitors 100% of an AR network's customer communications, marketing assets and partner activity, with every alert linked to the specific regulatory rule it engages and every override logged with reasoning. The MI surfaces risk at the principal-firm level in real time, the financial-promotion approval queue runs against COBS / CONC / BCOBS / ICOBS / MCOB and the Consumer Duty consumer-understanding outcome simultaneously, and the platform feeds the artefacts the annual PS22/11 self-assessment depends on.

Sedric is a single AI compliance platform used by regulated firms across multiple financial-services verticals — banks and issuers, fintechs and neobanks, trading and securities firms, crypto platforms, and debt-collection operations. See the banks, fintech, trading, crypto, and debt-collection pages for vertical-specific positioning. Sedric was named to the 2026 RegTech100, raised a $18.5M Series A led by Foundation Capital with Amex Ventures. The platform sits alongside an organisation's existing AR register, complaints and F&P workflows rather than replacing them, integrating through an open API.

The use-case Sedric is uniquely well-suited to is the one most principals struggle with: monitoring what the AR is actually saying to customers and what the AR is putting in market, at 100% coverage rather than sample, with rule-mapped output the principal can defend in a supervisory visit. This is the capability that lets a principal scale an AR network without scaling its supervision team. For the related Consumer Duty integration see Consumer Duty compliance software.

Do we need ARM software if we have ten ARs? At ten ARs, spreadsheets and a structured SharePoint can technically operate the regime — if the firm is disciplined. The case for software is stronger at twenty-plus ARs, and unavoidable at fifty-plus.

Can our existing GRC platform be extended for AR oversight? Sometimes. The risk register and policy management capabilities transfer; the AR-specific workflow, the financial promotion approval and the communications monitoring usually do not.

How does ARM software handle data residency for AR communications? A well-architected platform handles UK GDPR-compliant capture, processing and retention, with regional data residency where required. Confirm the architecture in vendor evaluation.

Does the AR see the platform? Typically yes — the AR has a portal for attestations, FinProm submissions, training, document upload. The principal sees the oversight layer; the AR sees the workflow layer.

What is the implementation timeline? For a network principal, three to nine months end-to-end. Communications monitoring is the most variable component — capture readiness across the AR base drives it.

How does this interact with the SMCR? The platform supports the SMF holder's prescribed responsibility for AR oversight by producing the evidence base. It does not relieve the SMF of accountability. It evidences the discharge of accountability.

Can the platform support the s.166 process if we are subject to one? Yes — by producing the artefact base the skilled person requires. Principals that have continuous-monitoring evidence going into a s.166 are in a meaningfully stronger position than those who have to reconstruct it under deadline.

Sedric's appointed representative management capability — register, attestation, financial promotion approval queue, communications monitoring, MI dashboard and complaint integration — is built on the industry's first compliance-dedicated LLM and operates with every flag linked to the specific FCA rule and every override logged with reasoning. It is the platform that lets principal firms scale an AR network without scaling the supervision team. Book a demo.

Convert your static procedures into active AI controllers that protect your brand 24/7.

.svg)

Scale marketing compliance without slowing down.

![Featured image for 'Appointed Representative Onboarding Due Diligence Under PS22/11' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a0b81b607d79026a101d4f0_6a0b81b42977dd24cc410483_featured-rebrand-appointed-representative-onboarding-due-diligence.png)

![Featured image for 'FCA Appointed Representative Regime 2026: A Practitioner Overview' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a0b81b36d8f7c39c4904b88_6a0b81b1e2d5d4d84195e47b_featured-rebrand-fca-appointed-representative-regime-2026.png)

![Featured image for 'FCA Section 166 Appointed Representative Reviews: A Practitioner Guide' — Sedric branded [sedric-rebrand-v2]](https://cdn.prod.website-files.com/69a7e1717e5289161221dbf3/6a0b81b07639c633808ebcb6_6a0b81ae0e0f2f4d6b2b4ed3_featured-rebrand-fca-section-166-appointed-representative.png)