.svg)

What is marketing review?

Marketing review is the structured process by which compliance, legal, and marketing teams evaluate every piece of customer-facing content (ads, emails, landing pages, social posts, video, partner placements) against regulatory requirements, internal policy, and brand standards before publication. In regulated financial services, marketing review is a defensive control that protects the firm from regulator findings, fines, and reputational damage.

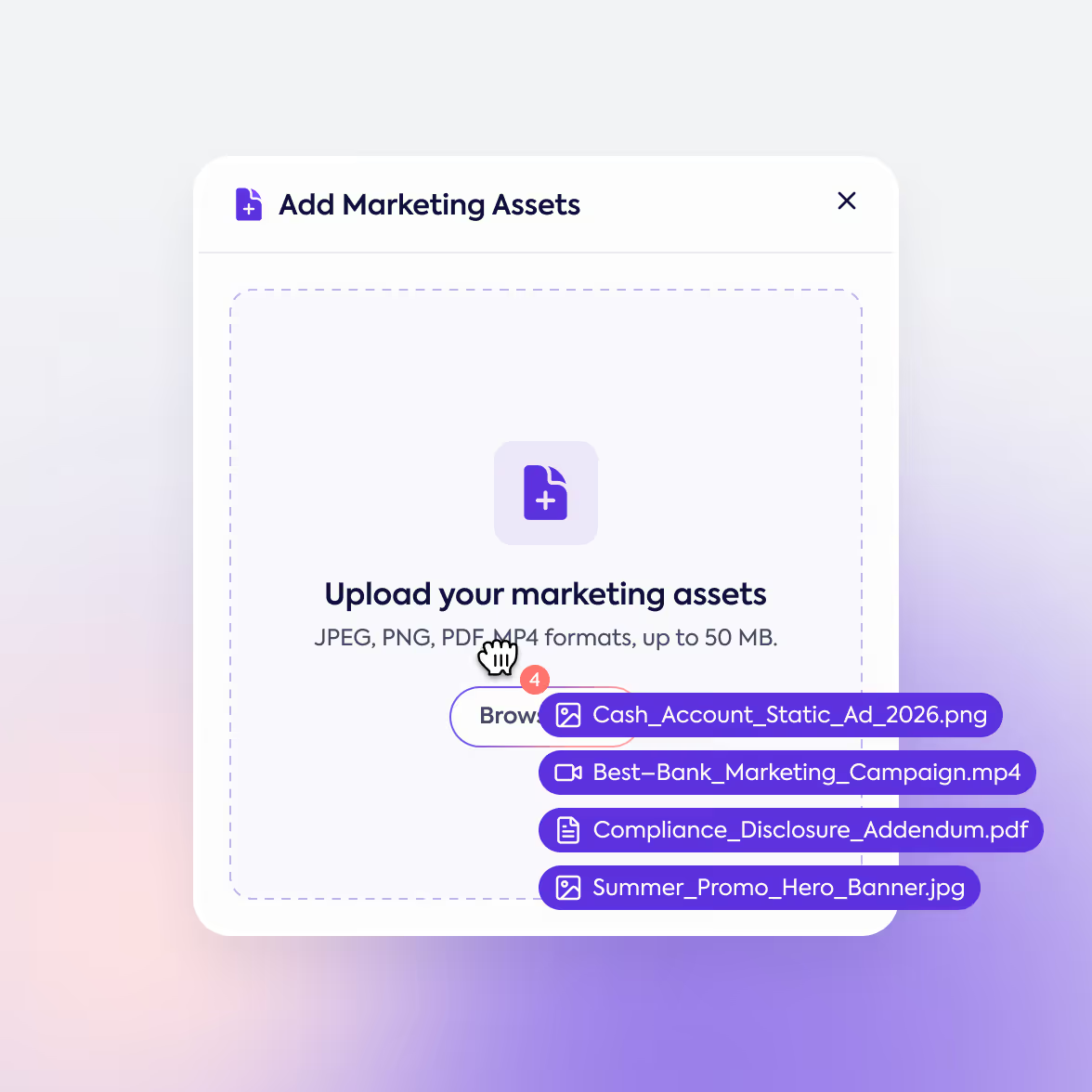

Modern marketing review covers four distinct surfaces: copy, design, video, and partner-published content. Each requires different review logic, different reviewers, and different evidentiary trails. The work scales with marketing volume. Every new product launch, channel, language, and partner expands the surface.

The output of marketing review is a binary: approved-for-publication or returned-with-edits. The supporting record (who reviewed, what they flagged, which policies applied, when it was approved) is what regulators ask for during exams.

Why marketing review matters in financial services

Financial services marketing operates under more regulatory scrutiny than any consumer-facing industry. UDAAP enforcement by the CFPB, FINRA Rule 2210 for broker-dealer communications, the SEC Marketing Rule for investment advisers, FCA COBS in the UK, and MiCA for crypto issuers all govern what firms can claim, how disclosures must appear, and how content must be retained.

The cost of failure is asymmetric. Single SEC enforcement actions for misleading marketing have exceeded $400 million. CFPB UDAAP findings can result in restitution programs that take years to unwind. Beyond fines, regulators increasingly require ongoing supervisory programs that consume compliance team capacity for years after a finding.

On the upside, firms that scale marketing review well ship 3 to 5 times more campaigns per quarter than peers. Speed-to-market on a new product, a new channel, or a new partner program is increasingly determined by review velocity, not creative velocity.

The marketing review process, end to end

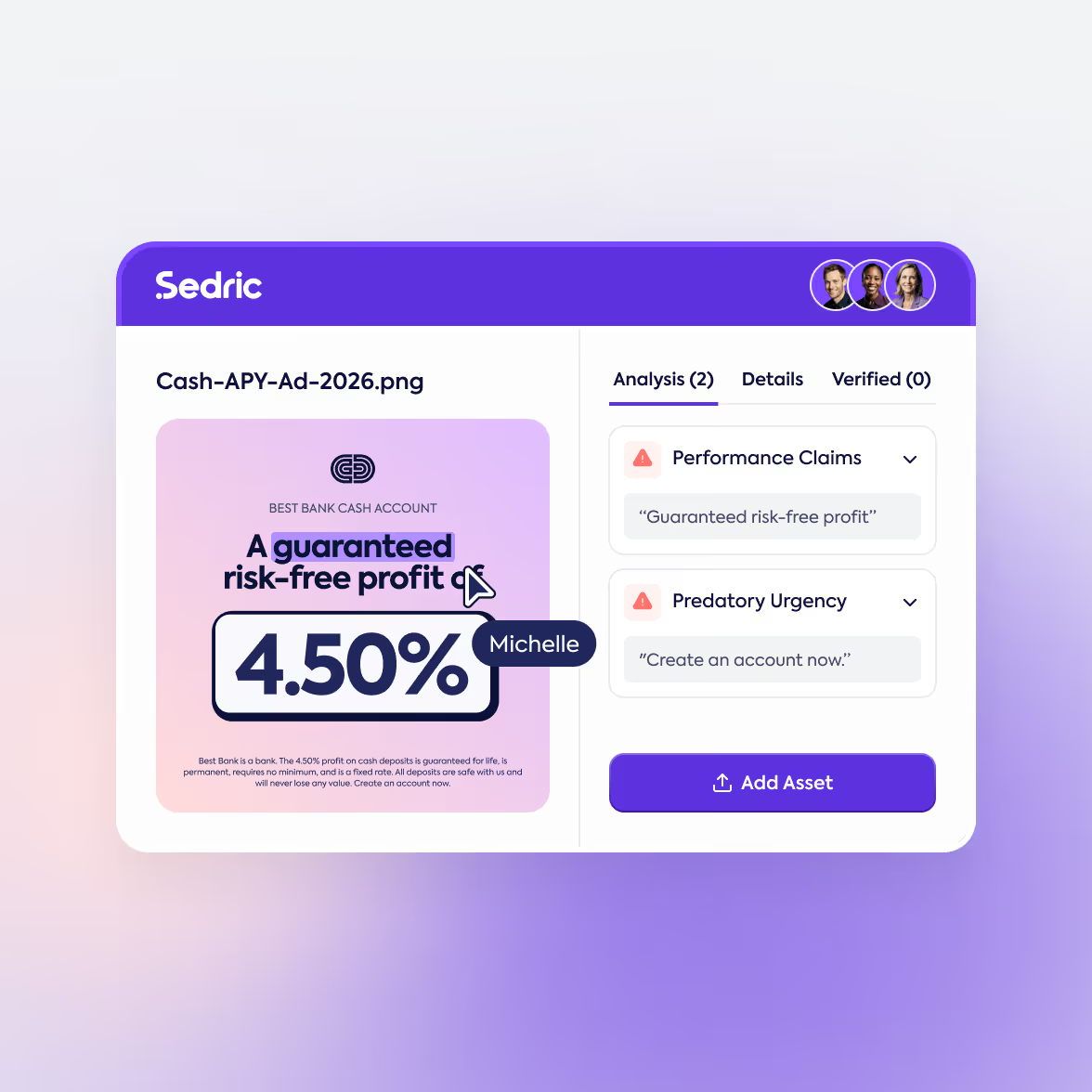

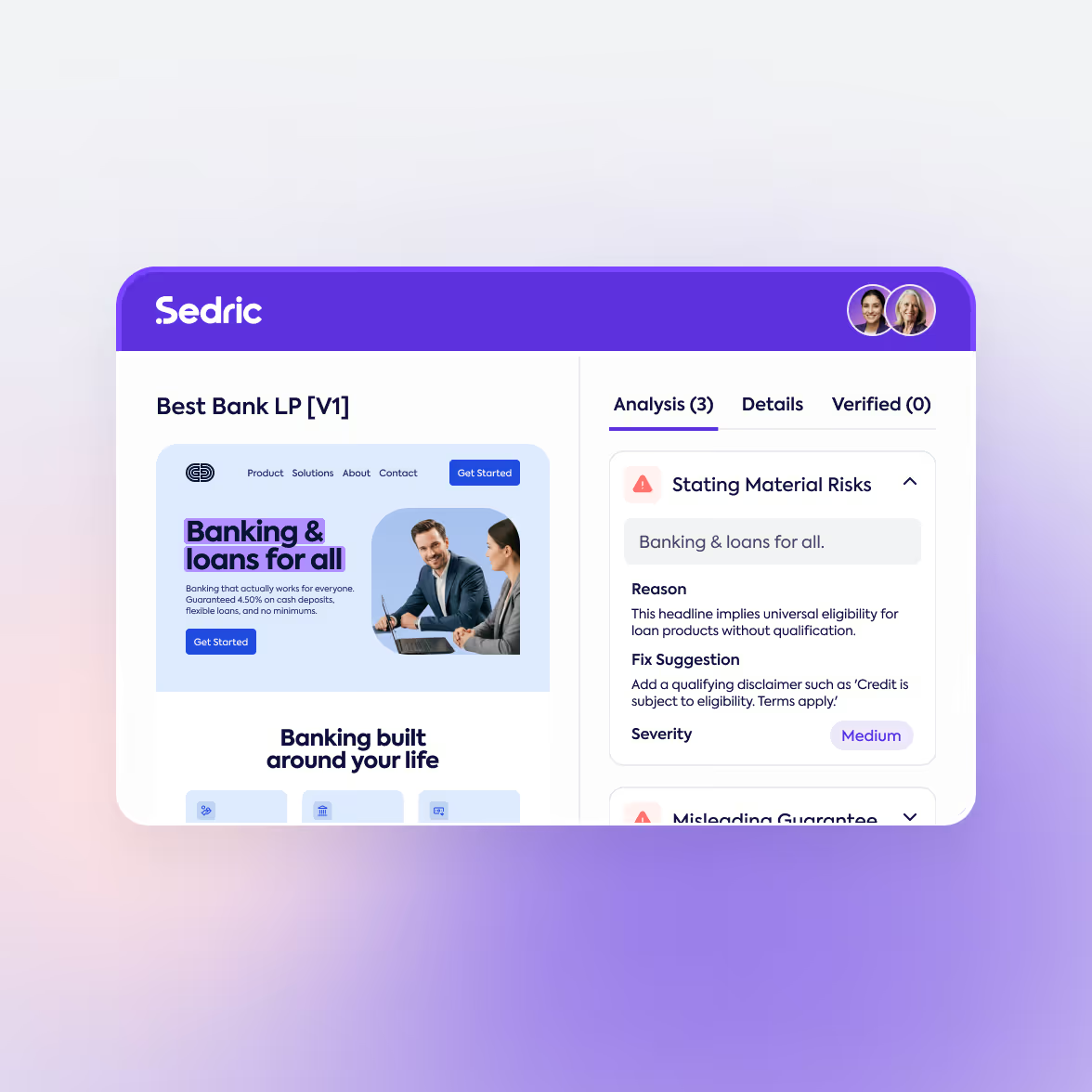

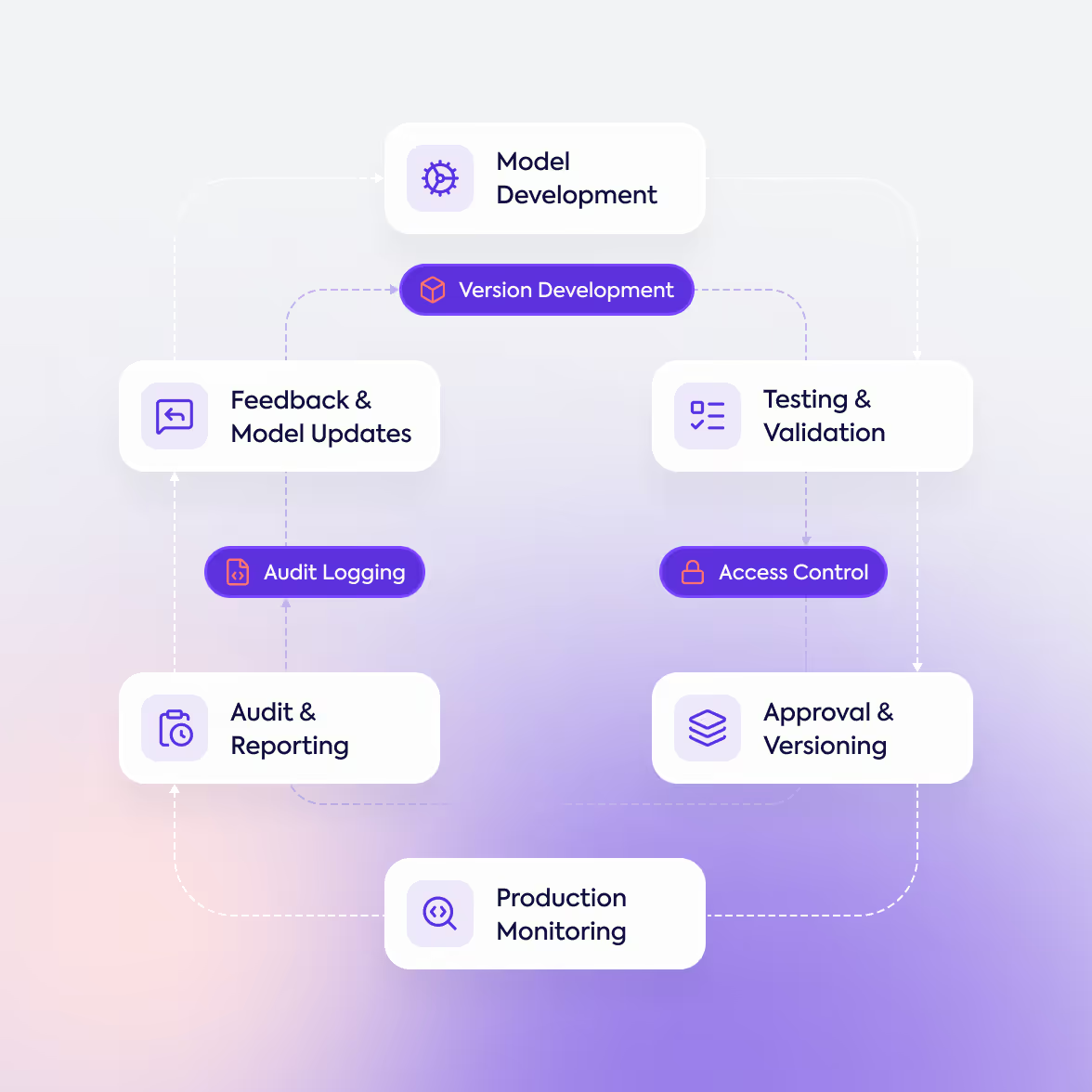

A modern marketing review workflow runs through five stages: brief (align on regulatory and policy constraints), draft (produce content with constraints embedded in templates and claims libraries), pre-review (automated scanning catches obvious violations like missing disclosures, prohibited language, banned claims, and brand drift), review and approve (compliance reviewers focus on judgment calls, not catching the basics), and monitor (after publication, automated systems scan for drift, partner violations, and policy changes that retroactively affect live content).

The biggest lever in this process is pre-review. When AI handles 80% of pattern-matching reviews automatically, compliance teams spend their time on the 20% that requires judgment, and approval cycles drop from days to hours. Each stage produces evidence: who briefed, what was drafted, what was flagged, what was overridden and why, what was approved, what changed post-publication. Together this is the audit trail regulators ask for.

Manual vs. AI-driven marketing review

Most regulated firms still review marketing manually. A creative is drafted, sent to compliance, reviewed by a human, returned with comments, revised, sent back. Cycle times average three to seven days per asset. Volume is bottlenecked by reviewer headcount. Coverage is partial. Many firms only review high-risk channels (ads, broker-dealer communications) and let others (social posts, partner content) ship without review.

AI-driven marketing review changes the baseline. Drafts are scanned against your policies and regulations the moment they are created. Flags arrive in seconds, with citations to the specific rule each violation triggers. Compliance reviewers see only the work that requires their judgment. Cycle times drop from days to minutes. Coverage extends to every asset, every channel, every partner. The defensibility of AI-driven review comes from explainability. Modern compliance AI shows exactly which policy or regulation triggered each flag, preserves a citation-linked audit trail, and supports the model risk management requirements (Federal Reserve SR 11-7, OCC Bulletin 2013-29) that bank regulators expect.

Marketing review at the speed of your business.

See how Sedric reviews your own marketing assets in seconds, with every flag mapped to the underlying regulation. 30-minute walkthrough on your content.

.svg)

.avif)

See how to automate your compliance

You’ll be able to see a full demo of marketing and communications compliance with your brand.